Illustration generated with AI assistance from Claude.

Summary — The Short Version

- A 401(k) is a retirement savings plan offered through an employer — contributions come out of the employee's paycheck automatically

- Contributions can be pre-tax (traditional) or after-tax (Roth), depending on the plan and the employee’s election, and both grow without annual taxes on dividends or capital gains

- Many employers add matching contributions — additional money deposited directly into the employee's account

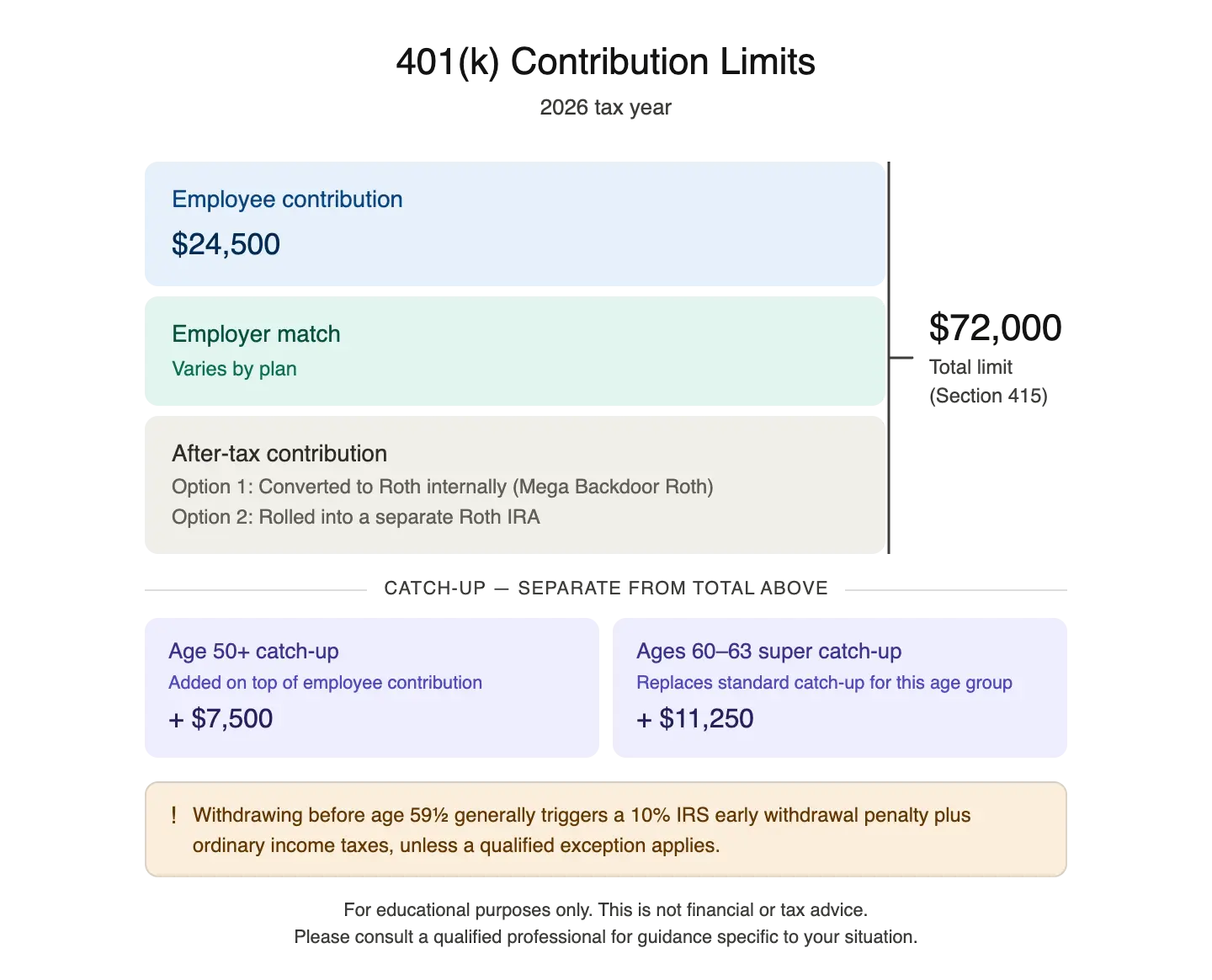

- For 2026, employees can contribute up to $24,500 — with additional catch-up amounts for those 50 and older

- The account is portable — it stays with the employee when changing jobs

- Before age 59½, withdrawals generally come with a 10% penalty in addition to applicable taxes, but exceptions exist

- Required Minimum Distributions begin at age 73 for traditional accounts

More detail below for those who want it.

The Basic Idea — In Plain Terms

A 401(k) is a retirement savings account that comes through an employer. The employee decides what percentage of their paycheck to contribute, and that money is automatically deducted before it lands in the employee's bank account — which makes saving the default, not the exception.

The money goes into investments — usually a selection of mutual funds or target-date funds offered by the plan. It grows over time, and the employee accesses it in retirement.

What makes it valuable is not just the investing — it is the tax treatment. Depending on which type of 401(k) is used, the employee either reduces taxes today or pays no taxes on the growth at all.

The Two Types: Traditional vs Roth

Most plans offer at least one of these, and many offer both:

Traditional (Pre-Tax) 401(k)

Employees contribute money from their paycheck before it is taxed. This reduces taxable income in the year of contribution — a meaningful benefit for those in a high tax bracket. The money grows tax-deferred, and ordinary income tax applies on withdrawals in retirement.

Roth 401(k)

Contributions are made with after-tax dollars — no deduction at the time of contribution. But qualified withdrawals in retirement — including all the growth — are completely tax-free.

Employees can often split contributions between traditional and Roth within the same plan year.

What Makes a 401(k) Particularly Valuable

Employer Match — Additional Compensation

Many employers match a portion of employee contributions — for example, contributing 50 cents for every dollar the employee puts in, up to a percentage of the employee's salary. This is additional compensation going directly into the employee's retirement account.

The employer match is very valuable components of a 401(k). Capturing the full match is generally worth prioritizing before other savings strategies.

One important nuance: how employee contribute can affect how much match they receive. Some plans calculate the match per paycheck rather than annually — and if employee max out their contributions early in the year before their final paycheck, they may miss match dollars. If the plan does not offer a "true-up" provision, spreading contributions evenly across all pay periods ensures the maximum match is captured. A previous post on this topic walks through how this can play out with real numbers.

Tax-Deferred or Tax-Free Growth

Inside a 401(k), dividends and capital gains do not create an annual tax bill. The money compounds without interruption — a structural advantage over a taxable brokerage account where investment income is taxed each year.

No Income Limits to Participate

Unlike Roth IRAs, which have income limits that phase out eligibility for high earners, there are generally no income limits to contribute to a 401(k). High earners who are phased out of direct Roth IRA contributions can still access Roth treatment through a Roth 401(k) at work, or through separate strategies like the Backdoor Roth IRA.

Portability

A 401(k) stays with the employee when changing jobs. It can typically be rolled into the new employer's plan or into an IRA. As long as it is handled as a direct rollover, there are no taxes or penalties.

2026 Contribution Limits

| Contribution Type | 2026 Limit |

|---|---|

| Employee contribution (traditional + Roth combined) | $24,500 |

| Catch-up contribution (age 50–59 and 64+) | +$7,500 |

| Super catch-up (ages 60–63) | +$11,250 |

| Total Section 415 limit (employee + employer + after-tax) | $72,000 |

A few notes on these limits:

- The $24,500 employee limit covers the combined total of traditional and Roth contributions — not each separately

- Catch-up contributions are in addition to the employee limit, not included within it

- The ages 60–63 super catch-up is a newer provision — for those in that age range, it replaces the standard catch-up with a larger amount

- The $72,000 Section 415 total limit includes employee contributions, employer matching, and after-tax contributions combined

Advanced Option: After-Tax Contributions and the Mega Backdoor Roth

Some 401(k) plans — not all — allow employees to make after-tax contributions beyond the standard $24,500 employee limit. These contributions do not receive the same pre-tax deduction as traditional contributions, but they open a potentially significant strategy.

If the plan also allows in-plan Roth conversions or in-service withdrawals, those after-tax contributions can be converted to Roth — either inside the plan or by rolling them out to a Roth IRA. This is sometimes called the Mega Backdoor Roth, and it can allow significantly more money to move into Roth account each year than the standard $7,000 Roth IRA limit.

The total room is limited by the $72,000 Section 415 cap. If an employee contributes $24,500 and receives $10,000 in employer match, approximately $37,500 in after-tax contributions remain possible — subject to the plan allowing it.

This strategy is not available in every plan. Whether it is available depends on the specific plan documents and whether the employer's plan was designed to permit it. A plan administrator can confirm whether this option exists in the plan.

"My Money Is Locked Up Until Retirement" — Not Quite

This is one of the most common misconceptions about 401(k) accounts.

Early withdrawals before age 59½ generally trigger a 10% IRS early withdrawal penalty on top of ordinary income taxes. This is a real cost.

However, several legitimate exceptions to the penalty exist:

- Rule of 55 — If an employee leaves their employer in or after the year they turn 55, distributions from that employer's plan may be available without the 10% penalty

- 72(t) distributions — Also called Substantially Equal Periodic Payments (SEPP), this allows early distributions under a specific IRS-approved schedule without penalty

- Qualified medical expenses — Unreimbursed medical expenses exceeding a threshold of the account holder's AGI may qualify

- Disability — Distributions due to total and permanent disability could be penalty-free

- Death — Beneficiaries who inherit a 401(k) are not subject to the early withdrawal penalty

- Certain hardship provisions — Plan-specific hardship withdrawals may qualify, though they are still subject to income tax

- Qualified Reservist Distributions — Certain distributions for military reservists called to active duty

Each exception has specific eligibility criteria and requirements. These should be evaluated carefully with a qualified tax or financial professional before taking action.

Later in Life: Required Minimum Distributions

Traditional 401(k) accounts are not tax-free — they are tax-deferred. Eventually, the IRS requires account holders to begin withdrawals. Beginning at age 73, Required Minimum Distributions (RMDs) mandate that a minimum amount be withdrawn each year from traditional accounts, calculated based on the account balance and life expectancy factors.

RMDs create taxable income regardless of whether the account holder needs the money — which can push retirees into higher brackets, affect Medicare premiums, and increase the portion of Social Security that is taxable.

Roth 401(k) accounts are currently subject to RMD rules as well — though rolling a Roth 401(k) into a Roth IRA at retirement eliminates the RMD requirement for Roth funds, since Roth IRAs have no lifetime RMD for the original account holder.

Managing the traditional versus Roth balance over a lifetime — including decisions about where to direct contributions and whether Roth conversions make sense in lower-income years — is one of the more nuanced but high-value aspects of retirement planning.

The Bottom Line

A 401(k) is one of the most accessible and tax-efficient tools available for building long-term wealth. The combination of automatic contributions, tax-advantaged growth, and employer matching makes it a foundation of most long-term financial plans.

But like most financial tools, the value depends on how it is used. Contribution timing, account type selection, match optimization, and the long-term balance between traditional and Roth accounts are all decisions that benefit from deliberate attention — not just a one-time setup.

Employees and investors with questions about how to maximize a 401(k) within the context of an overall financial picture could find that a comprehensive financial planning engagement is the right place to work through them.

This post is for educational purposes only and does not constitute individualized investment, tax, or legal advice. 401(k) plan rules vary by employer — not all features described here are available in every plan. Contribution limits are based on IRS guidance for the 2026 tax year and are subject to change. Early withdrawal rules and exceptions have specific eligibility requirements — consult a qualified tax professional before taking any early distribution. The Mega Backdoor Roth strategy is only available in plans that permit after-tax contributions and either in-plan Roth conversions or in-service withdrawals — confirm availability with your plan administrator. RMD rules are subject to legislative change. All investing involves risk, including the potential loss of principal. Advisory services offered through Trusted Path Wealth Management, LLC, an investment adviser registered with California. Registration does not imply a certain level of skill or training.