Blog | Trusted Path Wealth Management

No email list. No spam. Just visit when you're ready to read something good.

Why We Don't Use the Bucket Strategy for Retirement Income

The bucket strategy is a commonly discussed retirement planning framework — but we don't use it at Trusted Path Wealth Management. Here's what it is, why people like it, and why we believe a total return approach may serve retirees better.

Net Unrealized Appreciation: An Often-Overlooked IRS Provision for Company Stock in a 401(k)

When a 401(k) holds company stock that has grown significantly, an IRS provision called net unrealized appreciation may allow long-term capital gains rates to apply to a portion of the distribution — instead of ordinary income rates. Here is what NUA is, how it works, and the factors that affect whether it may be worth considering.

Four Layers of Tax Efficiency — What the Series Has Shown So Far

Four posts. Four independent illustrations of tax drag on a high-income California portfolio. Asset location, tax-loss harvesting, equity fund structure, bond type selection — each layer quietly reduces the tax bill year after year. Here's what the series has covered, why each layer compounds independently, and where it leads next.

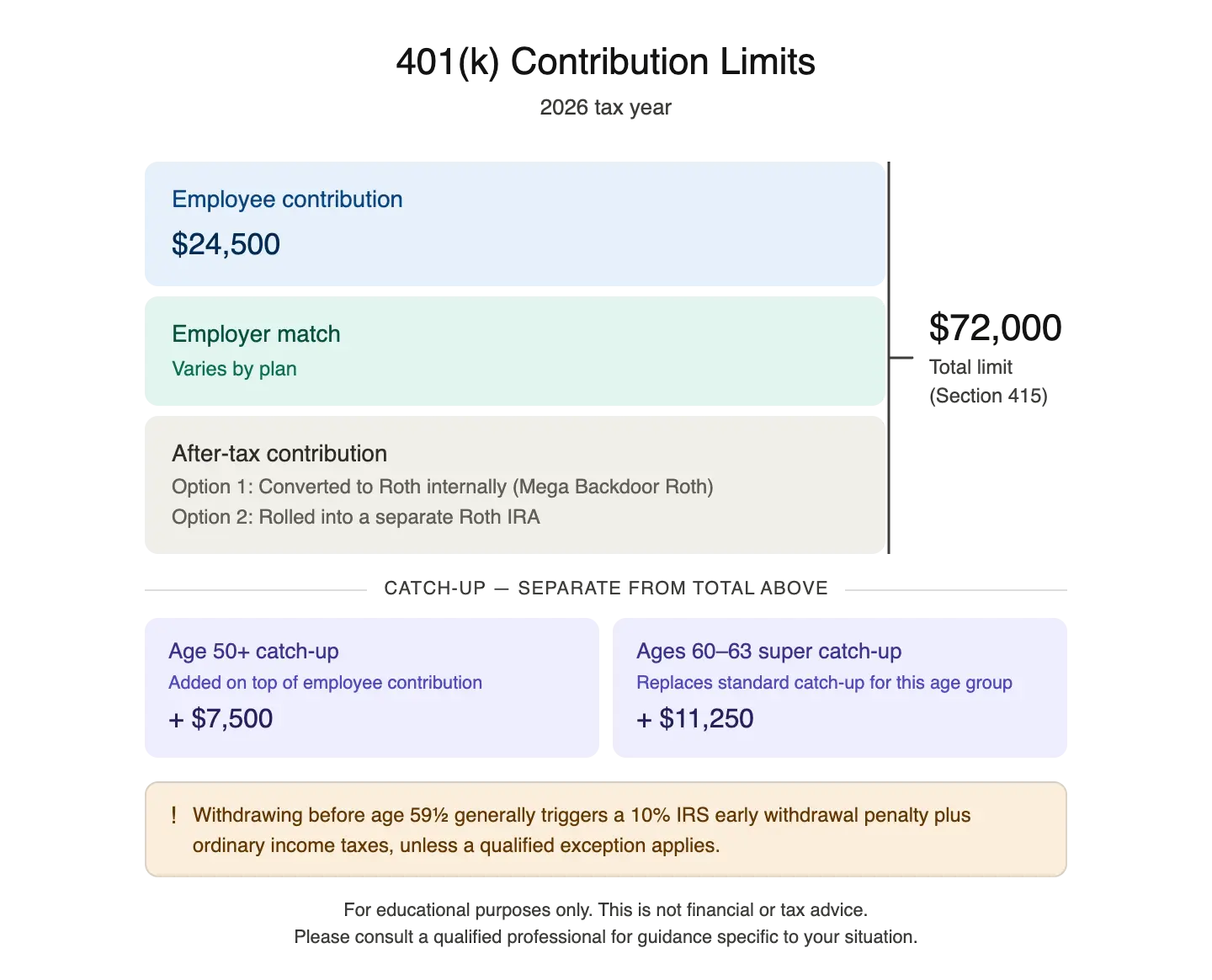

What Is a 401(k) and How It Works?

A 401(k) is one of the most powerful tools available for building long-term wealth — but most people only scratch the surface of how it works. Here is a straightforward look at what a 401(k) is, what makes it valuable, and common misconceptions about it.

The Bond That Pays Less but Keeps More: Tax Drag on Fixed Income Over 60 Years

A corporate bond paying 4% and a California municipal bond paying 2.75% — which one leaves a high-income Bay Area investor ahead after 60 years? The answer surprises most people. A deep look at how bond type affects after-tax returns, tax-equivalent yield, and why the highest-yielding bond is not always the best choice in a taxable account.

The Hidden Tax Drag on Stock Portfolio: How Fund Selection Alone Could Add $526,000 Over 60 Years

Two investors hold the same $100,000 in stocks. Same expected return. Same time horizon. But after 60 years, one has $526,000 more — without taking more risk or paying more. The only difference is how their stock funds handle dividends and foreign tax credits. A deep look at equity tax drag, qualified dividends, NIIT, and what fund structure means for after-tax outcomes.

The Quiet Strategy That Could Add $2.3 Million: Tax-Loss Harvesting Over a Lifetime

Tax-loss harvesting sounds technical. But for a high-income Bay Area couple starting at age 40, consistently applying it on top of a tax-efficient portfolio could add over $2.3 million by age 95 — without changing a single investment. Here's how it works, why it compounds the way it does, and what it means in practice.

One Change. $2.1 Million More. What Tax-Efficient Asset Location Does Over a Lifetime.

A hypothetical Bay Area couple makes one change to how their investments are placed across accounts — not what they own, not how much they save. Over 50 years, that single change compounds to $2.1 million. A step-by-step look at how tax-efficient asset location works, and why the gap keeps growing.

Why Maxing Your 401(k) Early Could Cost You Thousands in Employer Match

If your employer doesn't offer a 401(k) true-up provision, front-loading contributions could mean leaving significant employer match money on the table. Here's what to know.