For anyone researching retirement income strategies, the bucket strategy has probably come across their radar. It is a commonly discussed approach in retirement planning — featured in financial magazines, popular books, and advisor presentations everywhere.

It is easy to understand why people like it. It is visual, intuitive, and it feels safe.

But at Trusted Path Wealth Management, we don't use it — and we want to be transparent about why.

This post explains what the bucket strategy is, walks through its most commonly cited benefits, and shares the reasons we take a different path.

Image generated with Microsoft Copilot for educational purposes only.

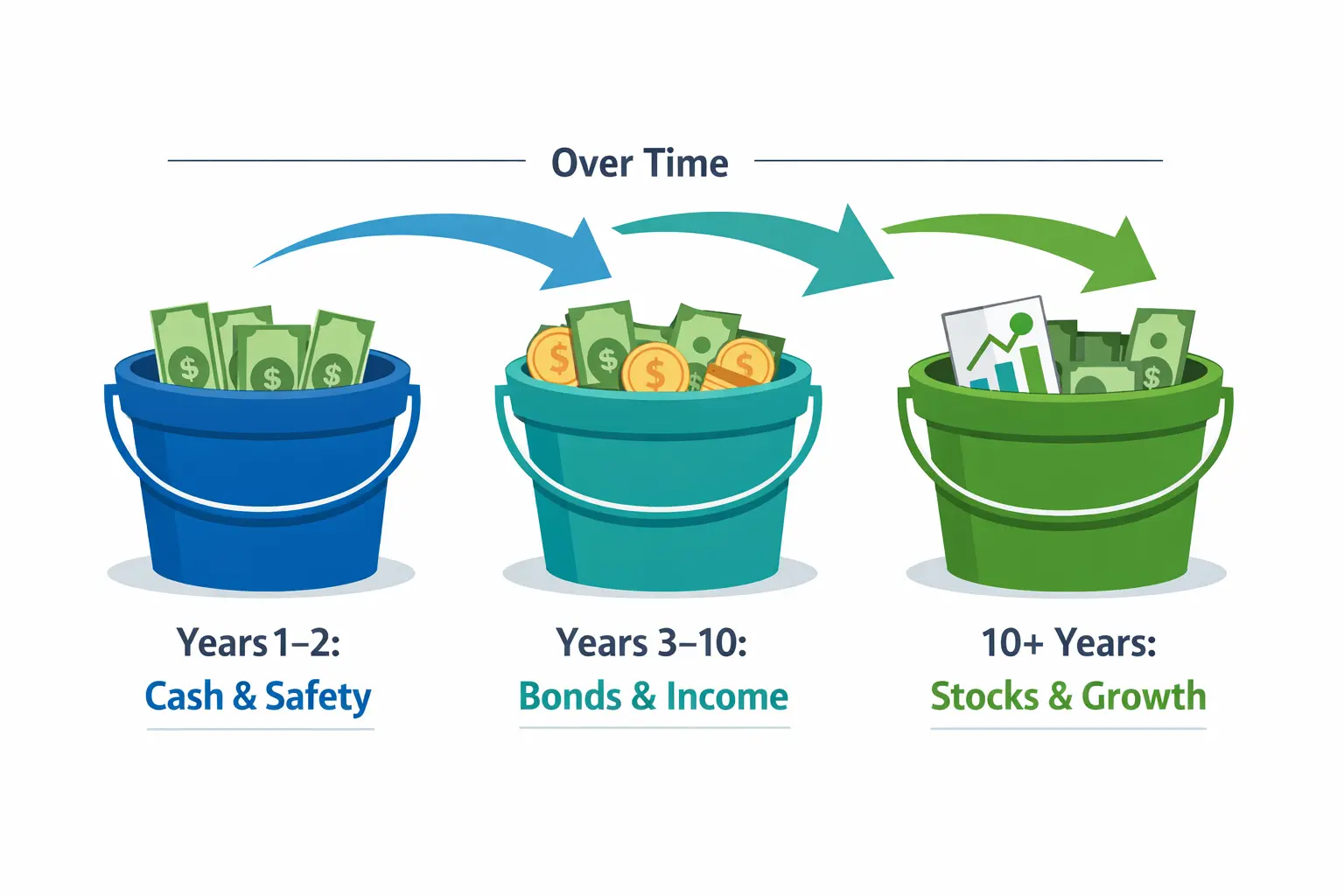

What Is the Bucket Strategy?

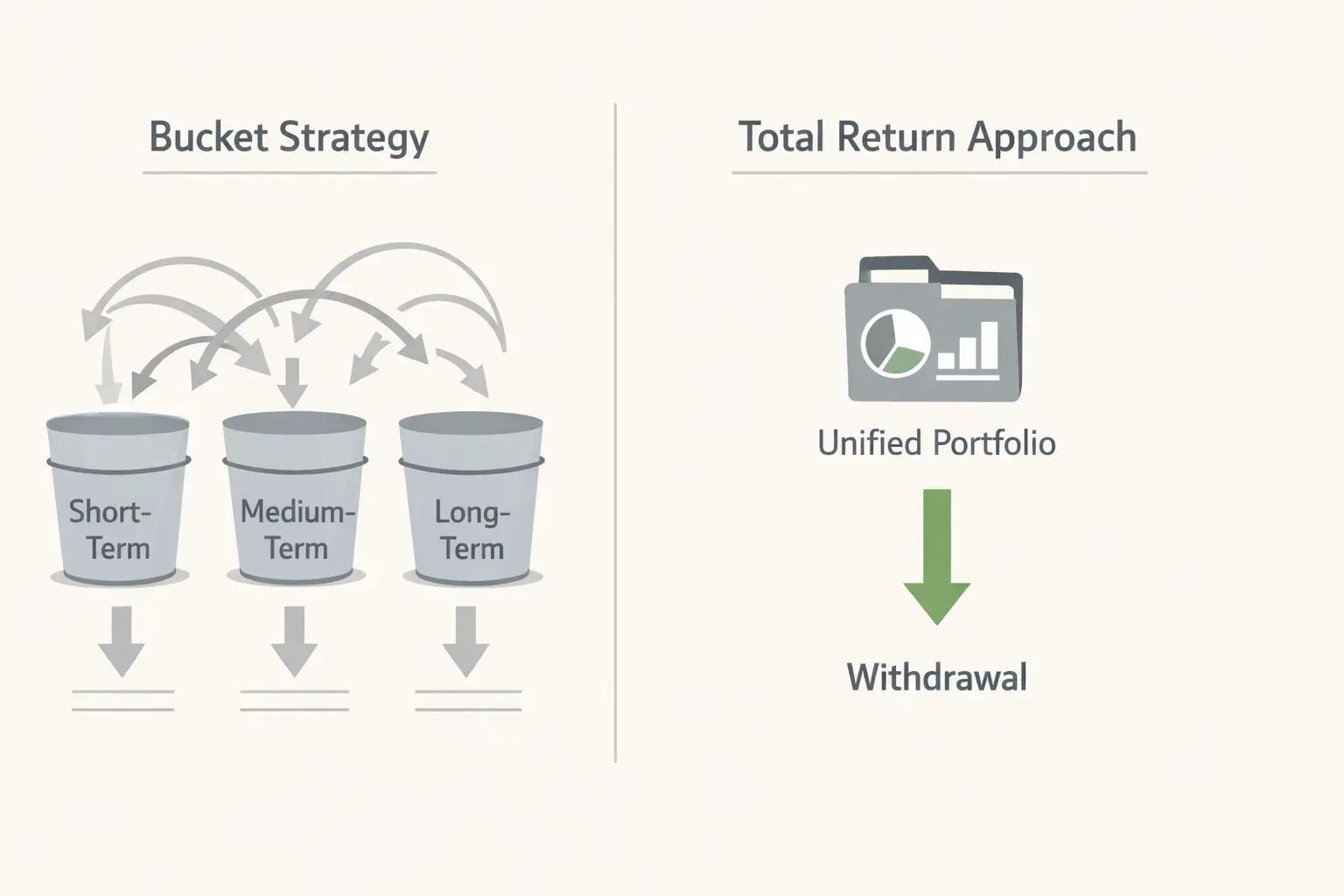

The bucket strategy is a retirement income approach where an investor divides their savings into separate "buckets," each one earmarked for a different time period.

A lot of versions describe three buckets:

- Bucket 1 — Right Now (Years 1–2): Cash and very safe accounts like money market funds or short-term CDs, set aside to cover near-term living expenses.

- Bucket 2 — Coming Soon (Years 3–10): Bonds and other conservative investments that refill Bucket 1 over time.

- Bucket 3 — The Future (10+ Years Out): Stocks and growth investments that have time to ride out market swings.

The logic goes like this: when the stock market drops, an investor doesn't panic-sell — they just live off Bucket 1 while the others have time to recover.

It is a comforting picture. Three labeled containers. Short-term safety on one side, long-term growth on the other.

Image generated with Microsoft Copilot for educational purposes only. This is a simplified illustration; actual retirement strategies depend on individual circumstances.

The Benefits the Bucket Strategy Offers — And Why We See It Differently

The bucket strategy has genuine appeal. Here are the most common reasons it resonates with retirees — and our honest perspective on each one.

Benefit 1 — "It gives investors peace of mind"

The claimed benefit: Knowing there are 1–2 years of cash set aside means a retiree won't lie awake worrying when the stock market falls. They can see their short-term money and feel secure.

Our perspective: We take near-term income security seriously — but rather than holding that money as idle cash, we use individual bonds in a rolling ladder when feasible.

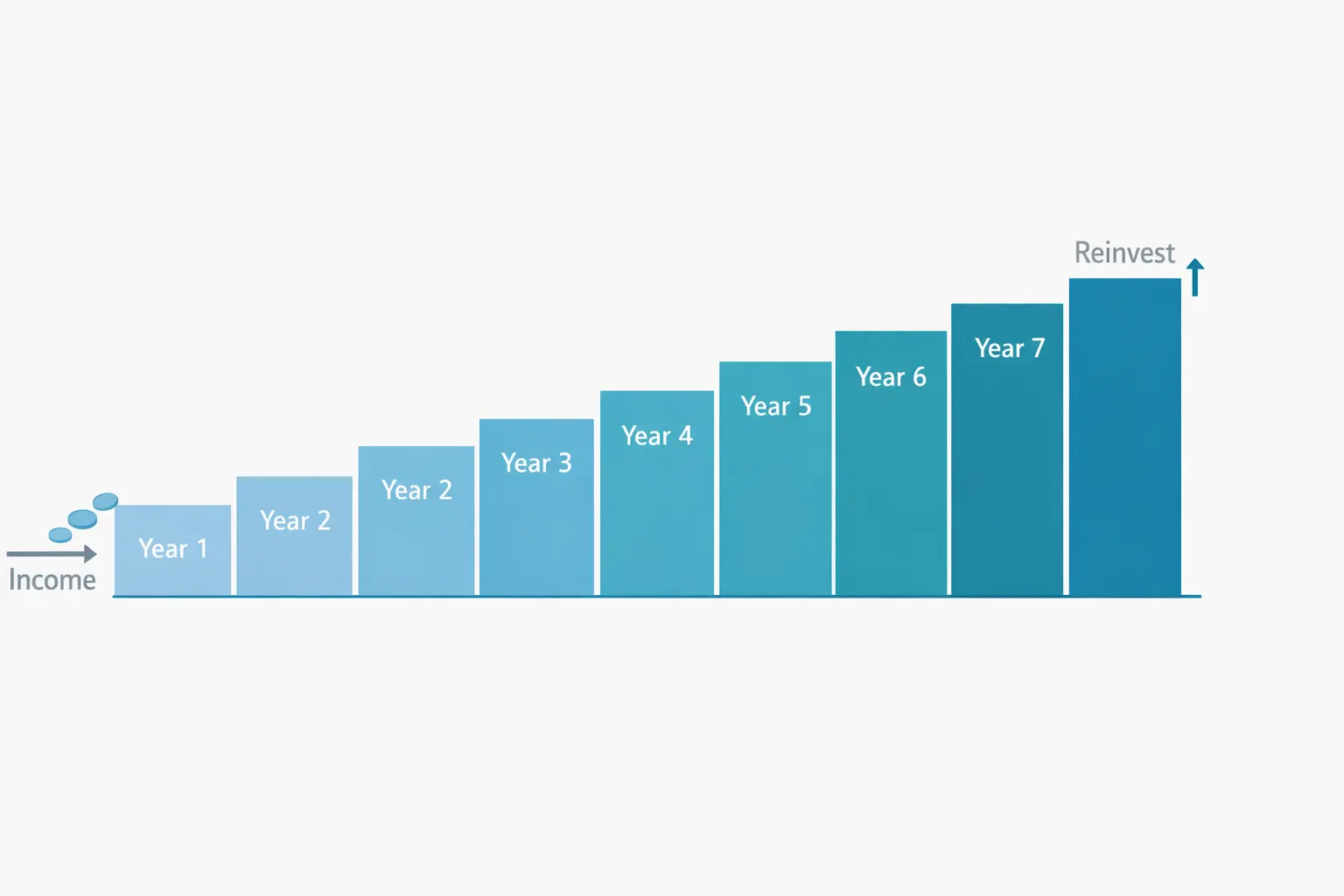

How a bond ladder works

A bond ladder is a set of individual bonds purchased with staggered maturity dates — for example, one bond maturing each year for the next 5 to 10 years. As each bond matures, the principal is available for income. Any portion not needed can be reinvested into a new longer-duration bond at the far end of the ladder, keeping it rolling forward.

- Short-term bonds serve the same purpose as a near-term cash bucket — a bond maturing in Year 1 or Year 2 is available when living expenses are due. A retiree has a predictable, year-by-year income floor built from maturing bonds rather than a low-yield cash account.

- Potentially higher interest than idle cash — by holding bonds across a range of maturities, there may be the potential to earn more than a money market or savings account. In many interest rate environments, longer-duration bonds tend to offer higher yields than very short-term instruments, reflecting what is generally known as the term premium. (Yield curves can vary; this is not guaranteed and interest rates may change.)

- Rolling the ladder forward — when the shortest bond matures and proceeds are used for income, a new bond is purchased at the longer end. This keeps the portfolio continuously exposed to longer durations where yield potential may be higher, rather than letting funds sit in cash awaiting deployment.

The result is similar near-term security to what the bucket strategy aims for — but with bonds working for the client while they wait, rather than cash earning lower interest than a bond ladder may potentially offer. And because each bond has a specific maturity date, there is no ambiguity about when funds become available, which is more precise than a generalized short-term bucket.

Image generated with Microsoft Copilot for educational purposes only. This is a simplified illustration; actual bond ladder strategies depend on individual circumstances, interest rates, and portfolio needs.

Benefit 2 — "It stops investors from panic-selling when markets drop"

The claimed benefit: Because Bucket 1 covers near-term needs, there is no need to touch stocks during a downturn. An investor can wait for markets to recover.

Our perspective: This is a behavioral goal — and it is a real one. Research consistently shows that panic-selling during market downturns is one of the most damaging things an investor can do.

But we address this same concern differently. Rather than adding structural complexity, we spend time upfront helping clients understand market history, build realistic expectations, and develop a written withdrawal plan. When someone has a clear picture of why their portfolio is built a certain way and what will happen in different scenarios, they are less likely to react emotionally — with or without labeled buckets.

Behavioral discipline, in our experience, comes from understanding — not from architecture.

Benefit 3 — "It's simple and easy to understand"

The claimed benefit: Three buckets are intuitive. Investors can picture their money in three containers. Almost anyone can understand it.

Our perspective: The concept is simple. The execution often isn't.

In practice, managing a bucket strategy raises a series of genuinely hard questions: How often should Bucket 1 be refilled? Should money be pulled from Bucket 2 or Bucket 3? What happens if both bonds and stocks are down at the same time? How should refills be coordinated with the client's tax situation? How should required minimum distributions (RMDs) be handled?

Different advisors answer these questions differently, and there is no universal rule. That lack of consistency can lead to decisions that are difficult to optimize or explain.

The refill-timing problem: an unsolved coordination question

Consider just the question of when to refill Bucket 1. There are three common answers — and each one introduces its own failure mode:

| Approach | How It Works | Failure Mode |

|---|---|---|

| Calendar-based | Refill on a fixed schedule (e.g. every January) | Forces a sale regardless of market conditions. Over a 25-year retirement, a fixed schedule will almost certainly coincide with a downturn at some point — the calendar does not know what markets are doing. |

| Threshold-based | Refill when Bucket 1 drops below a set level (e.g. 6 months of expenses) | During downturns the threshold approaches while assets are at their lowest — still forcing a loss-generating sale. During bull markets, easy refills can quietly encourage holding more equity than is appropriate: the equity-creep problem described in Benefit 5. |

| Opportunistic | Refill when markets seem favorable | The decision is governed by judgment rather than a systematic trigger — which may quietly turn a withdrawal plan into a market-timing strategy. |

No version of the bucket strategy specifies which of these approaches is correct — there is no consensus answer in the financial planning literature. The strategy is more of a conceptual framework than a defined process, and the operational decisions it leaves open may be genuinely unresolved.

A well-designed total return portfolio with a documented withdrawal strategy may actually be simpler to operate and explain — because the rules are clear and consistent from the start, and do not depend on one asset class being available to rescue another.

Benefit 4 — "It matches spending to the right time horizon"

The claimed benefit: By putting long-term money in growth investments, stocks have the time they need to recover from downturns. Near-term expenses are always covered.

Our perspective: This is how any well-diversified retirement portfolio works — with or without the bucket label.

A properly constructed portfolio already accounts for time horizons through its overall asset allocation. The question of how much to hold in stocks versus bonds versus cash is the real decision — and that decision should be driven by the investor's income needs, tax situation, risk tolerance, and retirement timeline, not by which labeled container the money sits in.

The bucket framework adds a layer of mental accounting around a process that good portfolio construction already handles.

Benefit 5 — "It protects investors from sequence of returns risk"

The claimed benefit: One of the biggest risks in early retirement is being forced to sell investments right after a bad market year. The bucket strategy protects against this by keeping near-term spending in cash.

Our perspective: Sequence of returns risk is real — in our view, it is one of the most significant financial risks a retiree faces, and we agree with that assessment completely. A bad sequence of returns in the early years of retirement can do lasting damage to a portfolio that a later recovery cannot fully undo.

That is precisely why we build an age- and investor-specific asset allocation for each client — because the asset allocation is the real protection against this risk, not the bucket label.

Here is a risk the bucket strategy can quietly introduce. As Bucket 1 and Bucket 2 are drawn down to fund spending, the equity in Bucket 3 — if it has not yet recovered — represents a growing share of what remains in the total portfolio. No one added more equity; the stable assets were simply spent. The longer equity stays depressed and the longer fixed assets continue to be depleted to cover expenses, the more equity-heavy the overall portfolio quietly becomes. A retiree who started with a moderate allocation may find, a few years into a prolonged downturn, that their effective equity exposure has drifted well above what they originally intended — with less of the stable cushion remaining to absorb further losses.

A carefully constructed, investor-specific asset allocation is designed so that a retiree holds a level of equity they can genuinely sustain through a downturn — not a level they feel pressure to take on because a bucket needs to be refilled on a timeline.

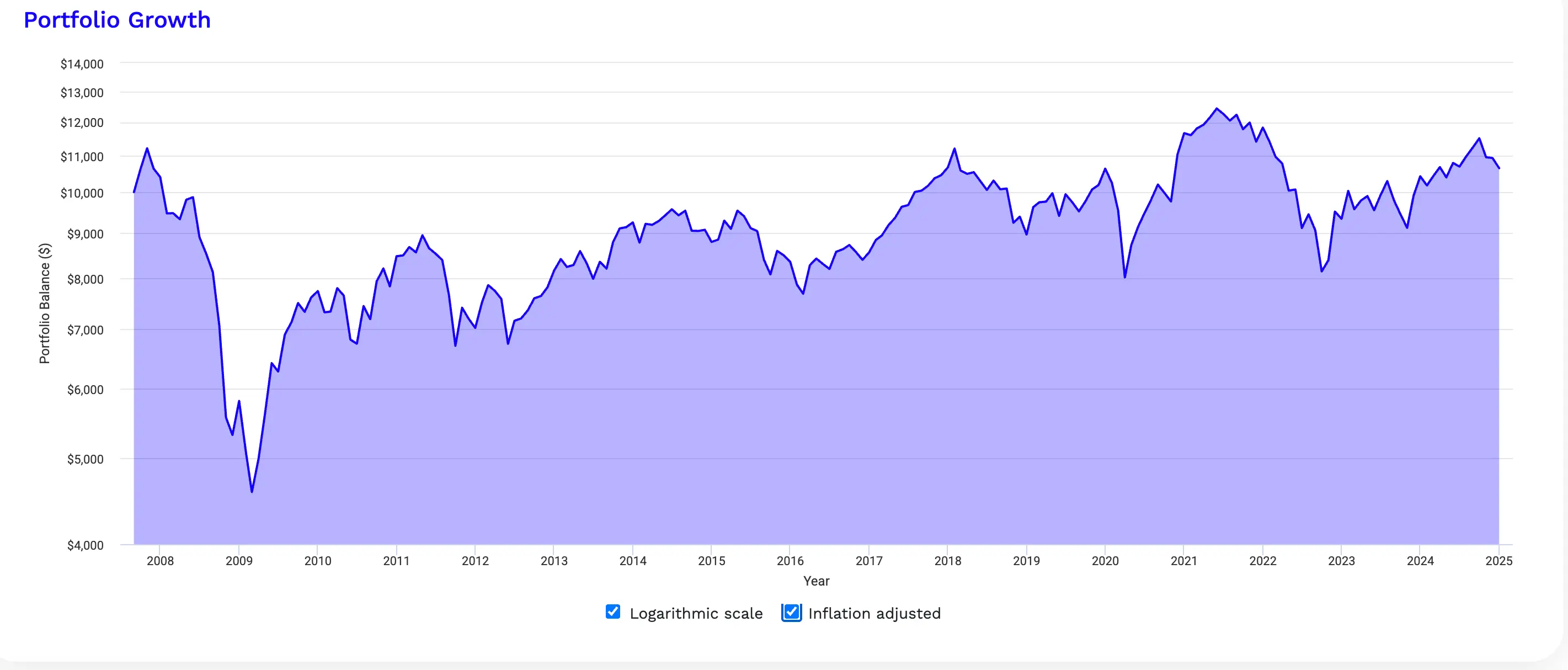

What History Suggests About Equity Recovery Timelines

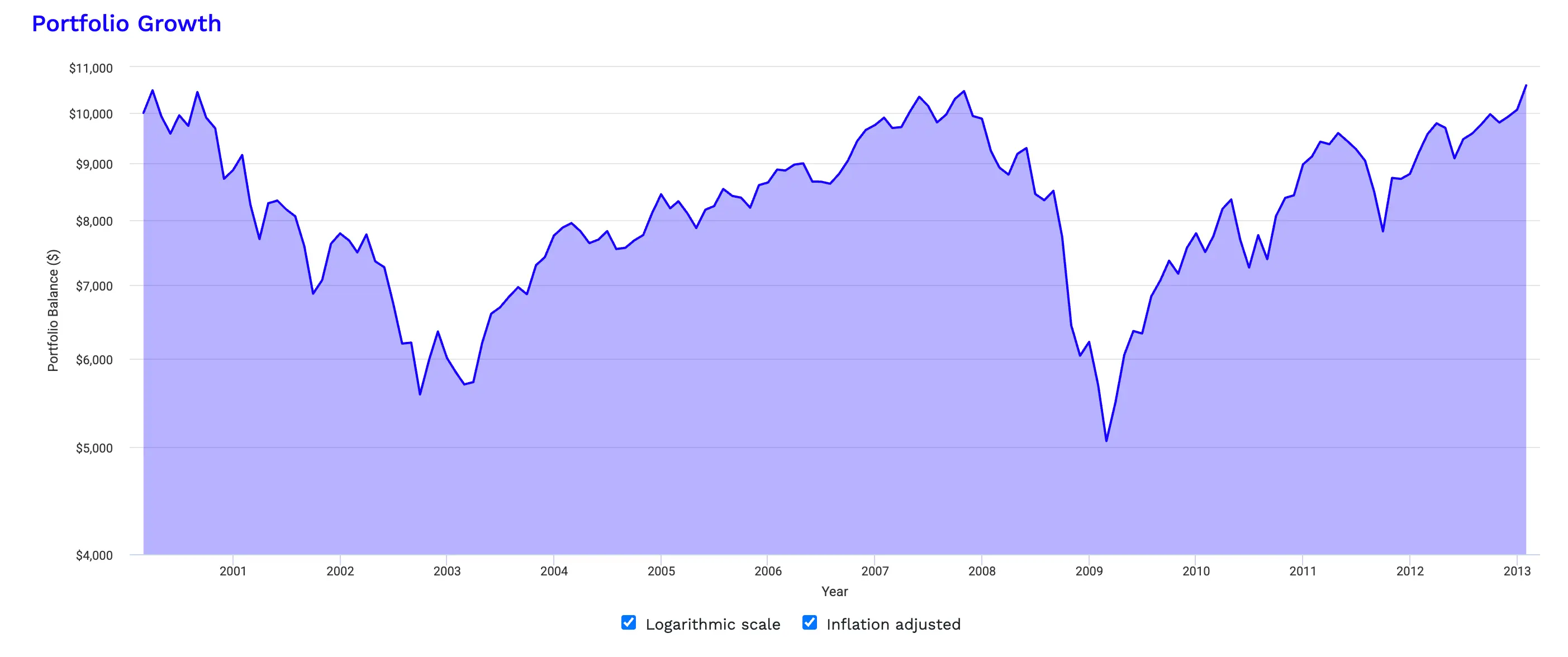

Per data from PortfolioVisualizer.com, an inflation-adjusted $10,000 invested in a broad U.S. equity portfolio in March 2000 — at the onset of the Dotcom crash — barely returned to its starting value by 2007. Before a retiree could take comfort in that recovery, the Subprime Crisis arrived and pushed the portfolio back down again. That same inflation-adjusted investment did not sustainably recover to its March 2000 level until January 2013 — 10+ years after the initial investment.

When tax drag on dividends is factored in — the taxes an investor would have owed on distributions received along the way — it took even longer to recover in true after-tax terms.

For a retiree relying on the bucket strategy during that period, the assumption that the long-term equity bucket would recover in time to refill the medium-term bucket simply did not hold. The recovery took far longer than the 3-to-10 year window the strategy is built around. There was no opportunity to refill buckets on the timeline the approach assumes.

Source: PortfolioVisualizer.com. For educational illustration purposes only. Past performance is not indicative of future results.

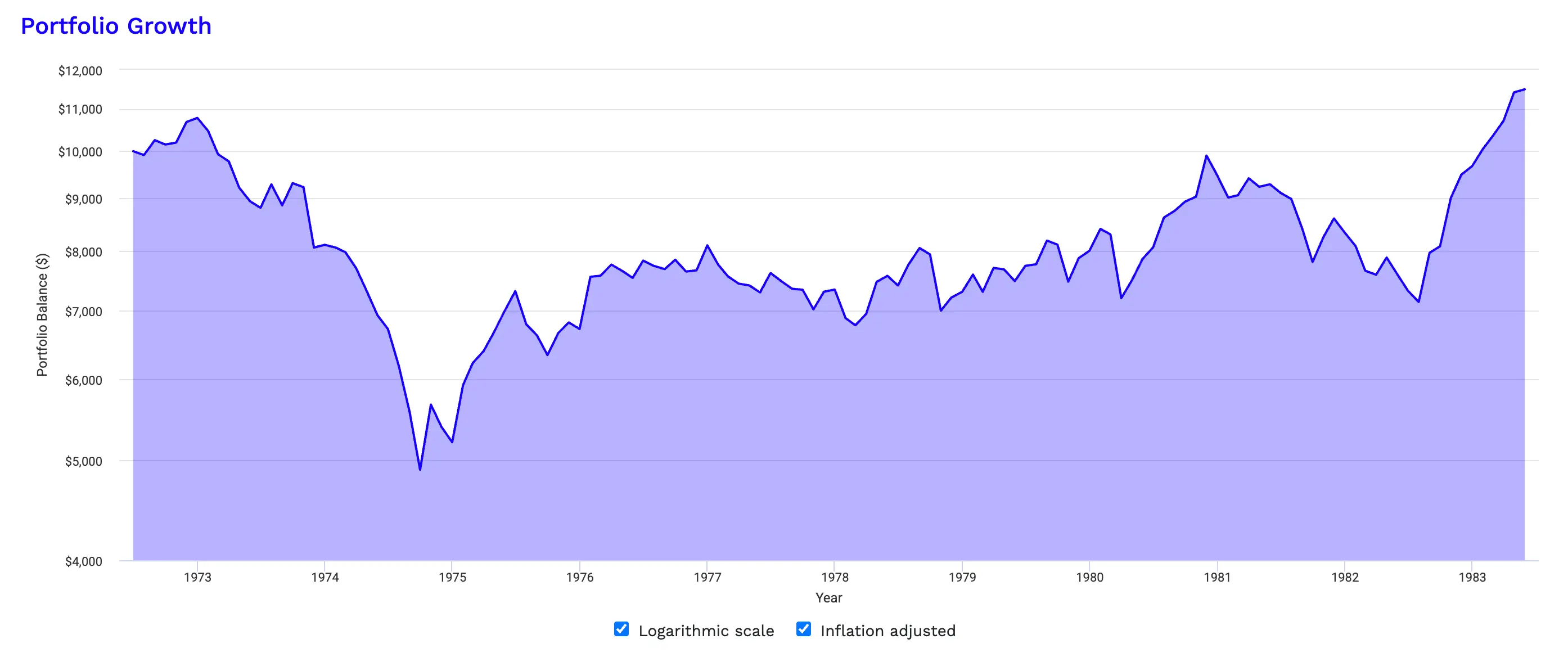

This was also not the first time U.S. equity investors faced a prolonged wait. Per data from PortfolioVisualizer.com, an inflation-adjusted $10,000 invested in a broad U.S. equity portfolio in July 1972 — just before the severe 1973–74 bear market driven by the oil embargo and stagflation — did not recover to its inflation-adjusted starting value until May 1983. That is 10+ years, during a period when high inflation was eroding purchasing power at the same time equity values were falling. A retiree who entered retirement in 1972 expecting the equity portion of a bucket strategy to recover and be available for refilling within a decade would have found the cupboard effectively empty for the entire decade of the 1970s.

Source: PortfolioVisualizer.com. For educational illustration purposes only. Past performance is not indicative of future results.

This is not an isolated U.S. example. Per data from PortfolioVisualizer.com, an inflation-adjusted $10,000 invested in a Global ex-U.S. Stock Market portfolio in September 2007 did not return to its starting value until the beginning of 2021 — 10+ years later. Before that recovery could be relied upon, the portfolio declined again within a year. It did not recover back to the inflation-adjusted $10,000 starting point until December 2024 — 15+ years after the original investment. That timeline does not include any tax drag on dividends received along the way, which would push the true after-tax break-even even further out.

A retiree who retired in September 2007 with international equity in their long-term bucket had no meaningful opportunity to refill any other bucket from that portion of their portfolio for 15+ years.

Source: PortfolioVisualizer.com. For educational illustration purposes only. Past performance is not indicative of future results.

We may never see a sequence like 1972–1983, 2000–2013, or 2007–2024 again — or we may see something that takes even longer to recover. The honest answer is that no one knows. And that is precisely why we do not believe in building a retirement income strategy around the assumption that equities will recover on any particular schedule. The bucket strategy may need that assumption most when markets are at their worst — and that is exactly when it is least likely to hold. We believe it is important to design a portfolio without assuming we know what lies ahead, building an asset allocation a client can genuinely sustain whether recovery comes in three years or twenty.

Data referenced from PortfolioVisualizer.com for educational illustration purposes only. Past performance is not indicative of future results. Individual results will vary based on portfolio composition, withdrawal rates, tax situation, and other factors. These periods were selected specifically to illustrate tail-risk scenarios in which inflation-adjusted equity recovery took unusually long. They are not representative of average or typical market recovery timelines, and other historical periods would show faster recoveries.

Our Concerns With the Strategy

At Trusted Path Wealth Management, we use a total return approach: one unified, thoughtfully constructed portfolio, paired with a clear and tax-coordinated withdrawal strategy.

Here is the core issue with the bucket strategy as we see it:

A portfolio doesn't know which bucket it's in.

A portfolio is one interconnected system. Putting mental labels on different portions of it doesn't change the math. What changes outcomes is the total asset allocation, the withdrawal sequence, and how well the strategy is coordinated with the client's taxes, Social Security timing, RMDs, and estate goals.

When we look at the bucket strategy through that lens, we see several practical concerns:

- Cash drag — Holding 1–2 years of expenses in near-zero-yield cash may quietly erode purchasing power over a long retirement. The cost is easy to underestimate — until it is quantified.

- Tax coordination is harder — Bucket-based systems often don't address which account type (IRA, Roth, taxable brokerage) withdrawals should come from — a major driver of tax efficiency

- Rebalancing gets complicated — Deciding when and how to refill buckets requires ongoing judgment calls that may create unnecessary taxable events or leave the portfolio out of balance

- False sense of security — The buckets may provide psychological comfort while the underlying risk profile of the full portfolio still determines outcomes

- Arbitrary bucket sizes — How much goes in each bucket is often based on rough rules of thumb rather than a client's specific tax situation, income needs, and account mix

What cash drag actually costs — a hypothetical illustration

Assume a retiree holds a two-year expense buffer of $120,000 in a savings account yielding 1%. That earns $1,200 a year. The same $120,000 deployed in a short-term bond ladder yielding 4% earns $4,800 — a gap of $3,600 every year.

Over a 25-year retirement, that $3,600 annual shortfall, if instead compounded at the same 4% bond yield, grows to roughly $150,000 in foregone wealth. Even without any compounding, the simple running tally is $90,000.

For illustrative purposes only. Actual yields, inflation, and portfolio outcomes will vary. This example does not represent any specific investment product or guarantee of return.

What the research literature finds

The concerns above are not simply a house view. Researchers and practitioners who have examined bucket strategies rigorously tend to reach a consistent conclusion.

Michael Kitces — one of the most widely cited voices in retirement planning practice — has written extensively that a bucket strategy and a total-return-with-systematic-rebalancing approach built on the same underlying asset allocation tend to produce materially similar portfolio outcomes. The math, he argues, is effectively the same: what the bucket framework calls "refilling" is functionally equivalent to rebalancing toward a target allocation. The bucket labels reorganize how a retiree thinks about the portfolio, not how it actually performs. (Managing Sequence-of-Return Risk With Bucket Strategies Vs. A Total Return Rebalancing Approach — Kitces.com)

Javier Estrada, a finance professor whose research has compared a range of retirement withdrawal strategies across long historical periods, has similarly found that the choice of withdrawal methodology matters far less to portfolio longevity than the choice of underlying asset allocation. How much is in stocks versus bonds — and whether that mix is appropriate to the investor — is the primary driver of outcomes. (The Bucket Approach for Retirement: A Suboptimal Choice — Javier Estrada, IESE Business School, 2019)

The general finding across this literature: when the underlying allocation is held constant, bucket strategies do not demonstrate a measurable return advantage or longevity advantage over simpler total-return approaches. Where the bucket strategy does show a benefit, it tends to be behavioral — the mental framework helps some investors stay invested through volatility by making near-term spending feel more secure. That benefit is real. But it is a psychological benefit, not a mathematical one, and it is worth asking whether it is worth the operational costs — the cash drag, the tax coordination complexity, and the refill-timing problem — described above.

References to researchers and their work are provided for informational context. Readers are encouraged to consult primary sources. The research landscape on retirement income strategies continues to evolve.

Image generated with Microsoft Copilot for educational purposes only. Individual outcomes vary based on circumstances.

What We Do Instead

Rather than dividing a portfolio into buckets, we build a single, diversified portfolio that reflects each client's actual time horizon, income needs, and risk tolerance. Then we layer a clear withdrawal plan on top — one that addresses:

- Which accounts to draw from first (taxable, tax-deferred, or Roth) to manage the tax bill year by year

- How to coordinate withdrawals with Social Security and RMDs to avoid unnecessary tax spikes

- How to stay invested through market volatility with realistic expectations and a written plan to refer back to

- How to rebalance in a tax-efficient way without triggering unnecessary capital gains

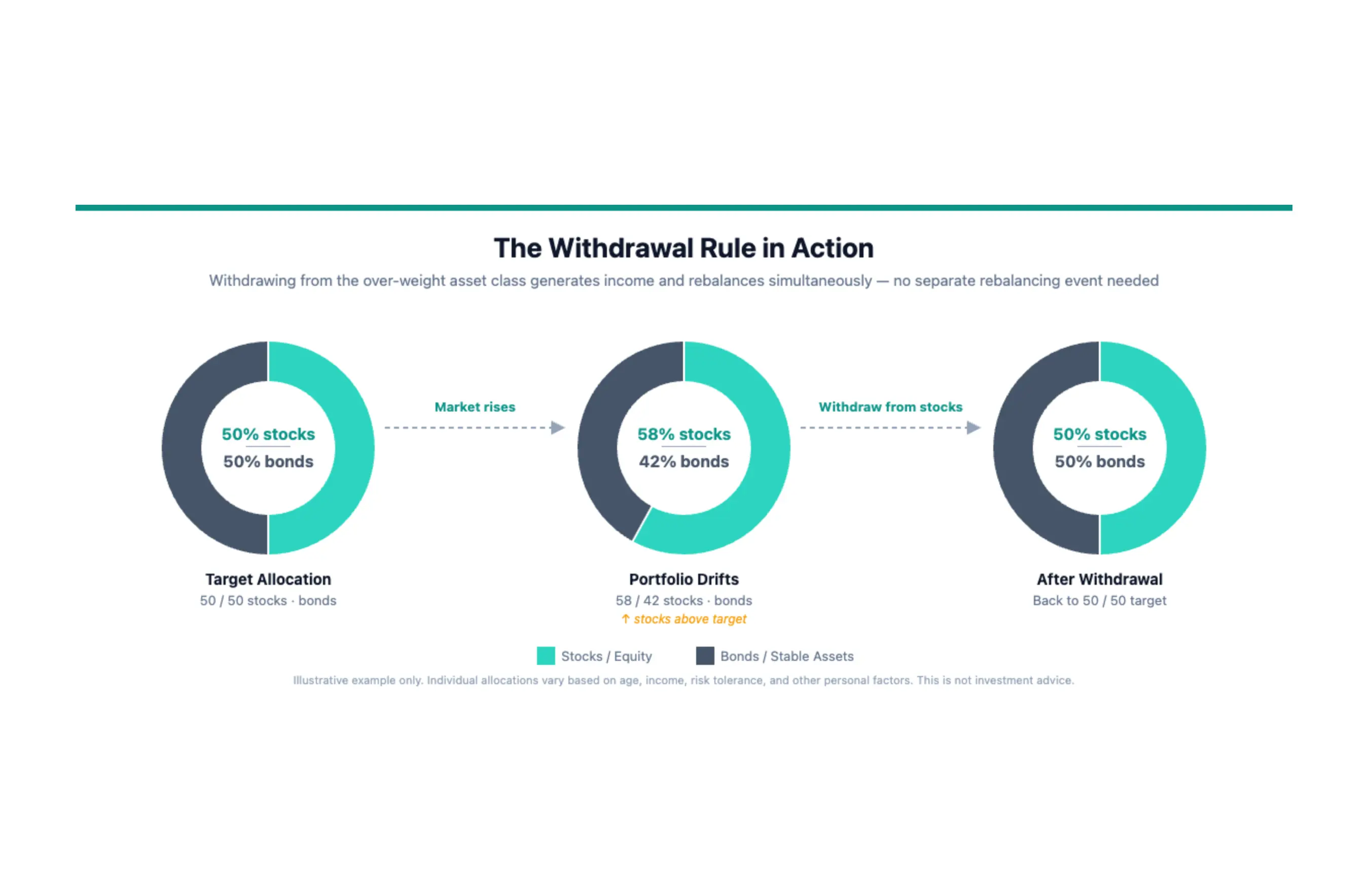

A Simple Withdrawal Rule Built Into the Asset Allocation

One concrete benefit of building an asset allocation around each client's personal characteristics — their age, income needs, risk tolerance, and time horizon — is that it creates a straightforward rule for how to take withdrawals in retirement:

Withdraw from whichever asset class is currently above its target allocation.

For example, if a client's target allocation is 50% stocks and 50% bonds, and after a strong equity market run their portfolio sits at 52% stocks and 48% bonds, the withdrawal comes from the stock side — bringing it back toward the target. If stocks have fallen and bonds are above target, withdrawals come from bonds instead.

This approach does two things at once: it meets the client's income need and it keeps the portfolio rebalanced without a separate rebalancing event. There is no judgment call about which bucket to tap or when to refill — the target allocation itself is the guide.

Compare this to the bucket strategy, where the decision of when to refill and from which bucket is left undefined and often handled differently by different advisors. With a target allocation and a simple withdrawal rule, the decision is systematic and repeatable every year.

This approach isn't less safe than the bucket strategy. In our view, it may be more disciplined — because the rules are consistent, the tax coordination is built in from the start, and there is no ambiguity about what to do when markets get volatile.

Illustrative example only. Individual allocations vary based on age, income, risk tolerance, and other personal factors. This is not investment advice.

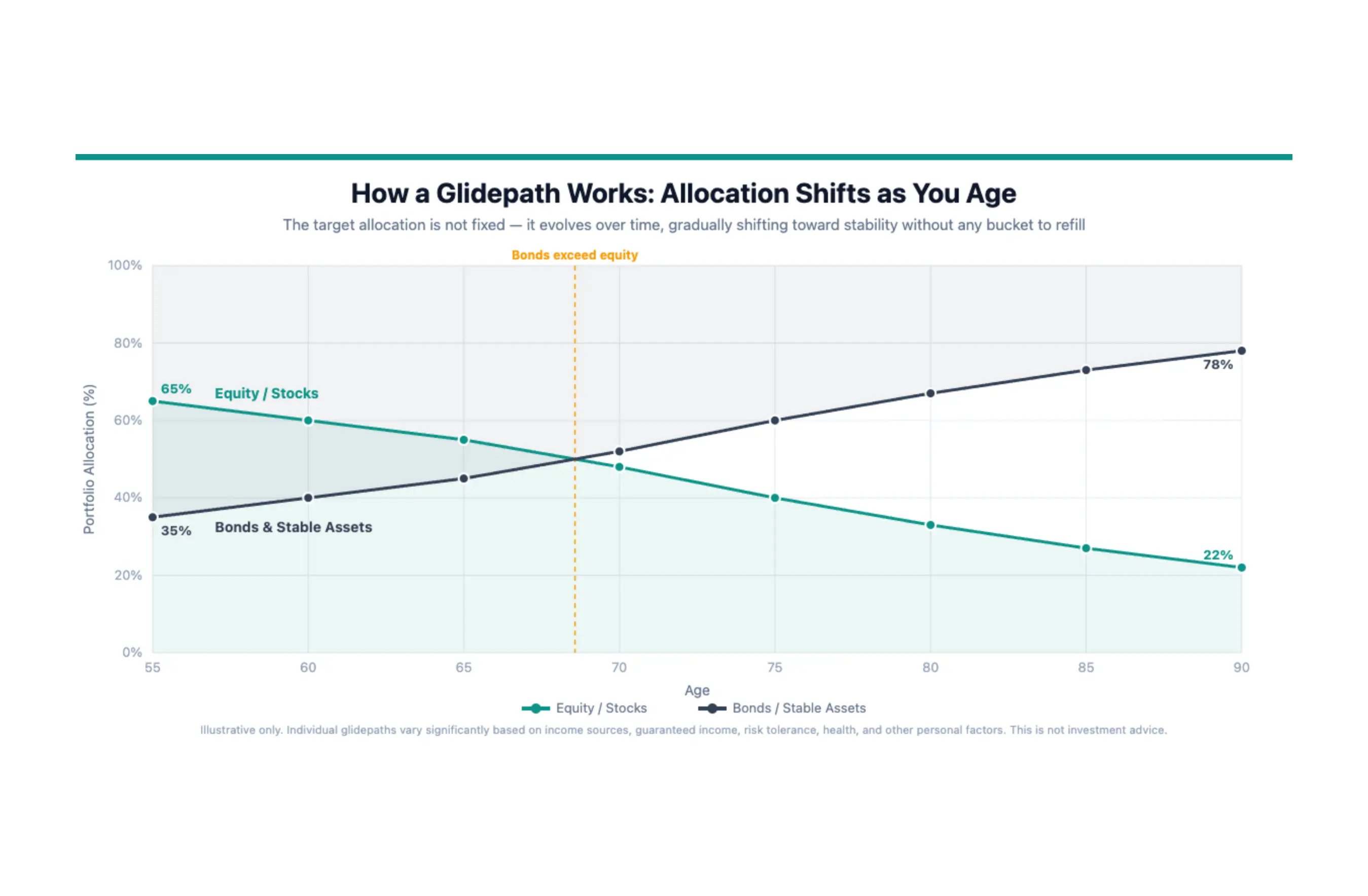

The Glidepath: How the Allocation Evolves Over Time

The target allocation isn't fixed for life. As a client ages deeper into retirement, the portfolio gradually shifts — typically toward a higher proportion of bonds and stable assets and a lower proportion of equity. This gradual shift is called a glidepath.

The glidepath is built around the client's specific situation: their age, expected longevity, income sources, and tolerance for volatility. A retiree at 65 with a pension and strong Social Security may carry more equity than a 65-year-old with no guaranteed income. A retiree at 80 may have shifted meaningfully toward fixed income.

This is the investor-specific, time-sensitive structure the bucket strategy tries to create through bucket sizing — but the glidepath achieves it systematically, with clear targets, and without the complexity of deciding when to refill anything.

Illustrative only. Individual glidepaths vary significantly based on income sources, risk tolerance, health, and other personal factors. This is not investment advice.

"But doesn't a bond ladder just recreate Buckets 1 and 2?"

It is a fair question, and the resemblance is real. A bond ladder holds short-to-medium-term fixed income that matures sequentially — which does sound similar to a bucket strategy's Bucket 1 (cash) and Bucket 2 (intermediate bonds). The distinction is structural, not cosmetic, and it matters in practice.

In the bucket strategy, the cash and bond holdings are mentally partitioned from the rest of the portfolio. The decision of when to draw from each partition, how and when to refill, and which bucket to tap is discretionary — there is no universal standard governing these choices. The cash in Bucket 1 sits explicitly separate, earning less than bonds by design, in order to feel psychologically insulated from market movements. That insulation is the source of both its comfort and its cost.

In a total-return approach with a bond ladder, the bonds are simply the fixed-income allocation — held because they earn more than idle cash while still maturing on a predictable schedule. There is no partition. The withdrawal decision is not "which bucket do I tap today?" but "which asset class is currently above its target allocation?" — the same rule in every market environment. The ladder provides the yield and the maturity structure; the allocation rule provides the discipline. No discretion, no refill timing problem, no incentive to let equity drift higher than appropriate.

The tax coordination difference compounds this. In a bucket framework, the decision of which account type to draw from — IRA, Roth, taxable brokerage — is typically separate from the bucket decision and often left undefined. In a total-return approach, both decisions are made together: withdraw from the above-target asset class, from the account that makes the most sense for taxes that year. One coordinated rule replaces two disconnected ones.

So yes — a bond ladder and the bucket strategy's Bucket 2 are both fixed income. But one is a component of an integrated portfolio governed by a systematic rule; the other is a discrete container managed by discretionary judgment. That is where the difference in execution complexity lives.

A note on individual needs: Every retiree's situation is different. If a bucket framework helps a client stay invested and avoid emotional decisions, that psychological benefit is real and shouldn't be dismissed. The goal is always a plan a client can stick to. What we want to avoid is a system that feels structured but creates hidden inefficiencies — particularly around taxes and long-term returns.

Where We Do Use Liability Matching — and Why It's Different

There is one related concept we do use selectively, and it is worth explaining because it often gets confused with the bucket strategy: liability matching.

What is liability matching?

Liability matching means setting aside a specific asset to cover a specific, known future expense — the asset and the obligation are paired together deliberately.

Think of it like booking a flight in advance. Rather than keeping a general "travel fund" bucket, a traveler sets aside the exact amount for a known flight, on a known date. The money is earmarked for that one thing.

In retirement planning, this might look like:

- Example 1 — The home repair: A retiree knows their roof is nearing the end of its life and expects to spend roughly $35,000 on replacement in about five years. Rather than holding that money in a general savings account or general portfolio, they could purchase a 5-year Treasury bond or CD today that will mature to approximately cover that cost. The asset is matched to the liability.

- Example 2 — The income gap: A client plans to delay Social Security until age 70, but retires at 64. That creates a six-year window where they need income from the portfolio. Rather than funding that from a generic "short-term bucket," we might structure a bond ladder — six individual bonds, one maturing each year — specifically sized to cover the annual income gap for each of those six years. Each bond covers a specific, known obligation.

How is this different from the bucket strategy?

The bucket strategy groups all retirement expenses into time-based containers — everything goes into one of three buckets regardless of what it's for. It is general by design.

Liability matching is precise by design. It identifies a specific future obligation — a known cost, a known date, a known amount — and matches a specific asset to it. There is no guesswork about when to refill or how much to hold.

| Bucket Strategy | Liability Matching | |

|---|---|---|

| What it covers | All expenses, grouped by time | One specific known expense |

| How precise | Approximate | Targeted |

| Good for | General income flow | Known, dated obligations |

| Cash drag risk | Yes — general cash buffer | Less — tied to a specific need |

We don't use liability matching for every expense — doing so would require holding far too many individual bonds and create its own complexity. But for large, well-defined future obligations — a planned home renovation, an income gap before Social Security, a known healthcare cost — it can be a disciplined and efficient tool layered on top of a total return portfolio.

It gives clients the precision they need for specific goals, without the broad inefficiency of labeling all their money into buckets.

Related Reading

- Smart Tax Strategies for RetirementPractical, tax-smart retirement strategies for California professionals and high-net-worth households. Learn how to mix account types, plan RMDs and withdrawals, use QCDs, and build a long-term tax-aware retirement plan.Read article →

- Top 5 Things High Earners Should Know About Retirement WithdrawalsDiscover the top 5 tips high earners need for smart retirement withdrawals—covering Social Security taxation, RMDs, Roth conversions, and common mistakes to avoid.Read article →

- A Step-by-Step Guide to Retirement PlanningLearn how to create a successful retirement plan with this retirement planning step by step guide, including clear goals, expense estimates, income strategies, investment planning, and ongoing adjustments. Start building your secure retirement today.Read article →

Closing Thoughts

The bucket strategy isn't wrong — it is a reasonable framework that helps many people think about retirement income. But frameworks are only as good as the decisions they produce.

At Trusted Path Wealth Management, we believe the best retirement income plan is one that is clearly connected to a client's goals, coordinated with their taxes, and built to hold up through decades of market uncertainty — not one that looks tidy on paper but creates complexity in practice.

Anyone interested in discussing how a total return approach might apply to their situation is welcome to schedule an introductory conversation. No cost or obligation. Scheduling does not establish an advisory relationship.

This content is for educational purposes only and does not constitute personalized investment, tax, or legal advice. Past performance is not indicative of future results. Please consult a qualified financial advisor and tax professional before making decisions based on this information.