Paying off debt is often treated as an obvious financial priority. But the reality is more nuanced, especially when it comes to student loans. While some borrowers focus on eliminating their student debt as quickly as possible, others take a more strategic approach: choosing not to pay it off aggressively, or in some cases, postponing payments entirely.

In certain situations, it may be appropriate to weigh other financial priorities alongside, or even ahead of, aggressively paying down student loans. As a fiduciary and fee-only financial planner in Santa Rosa, I don’t make one-size-fits-all recommendations. Instead, I help clients evaluate their full financial picture, and in some cases, that means student loans may not be the most urgent obligation to tackle first.

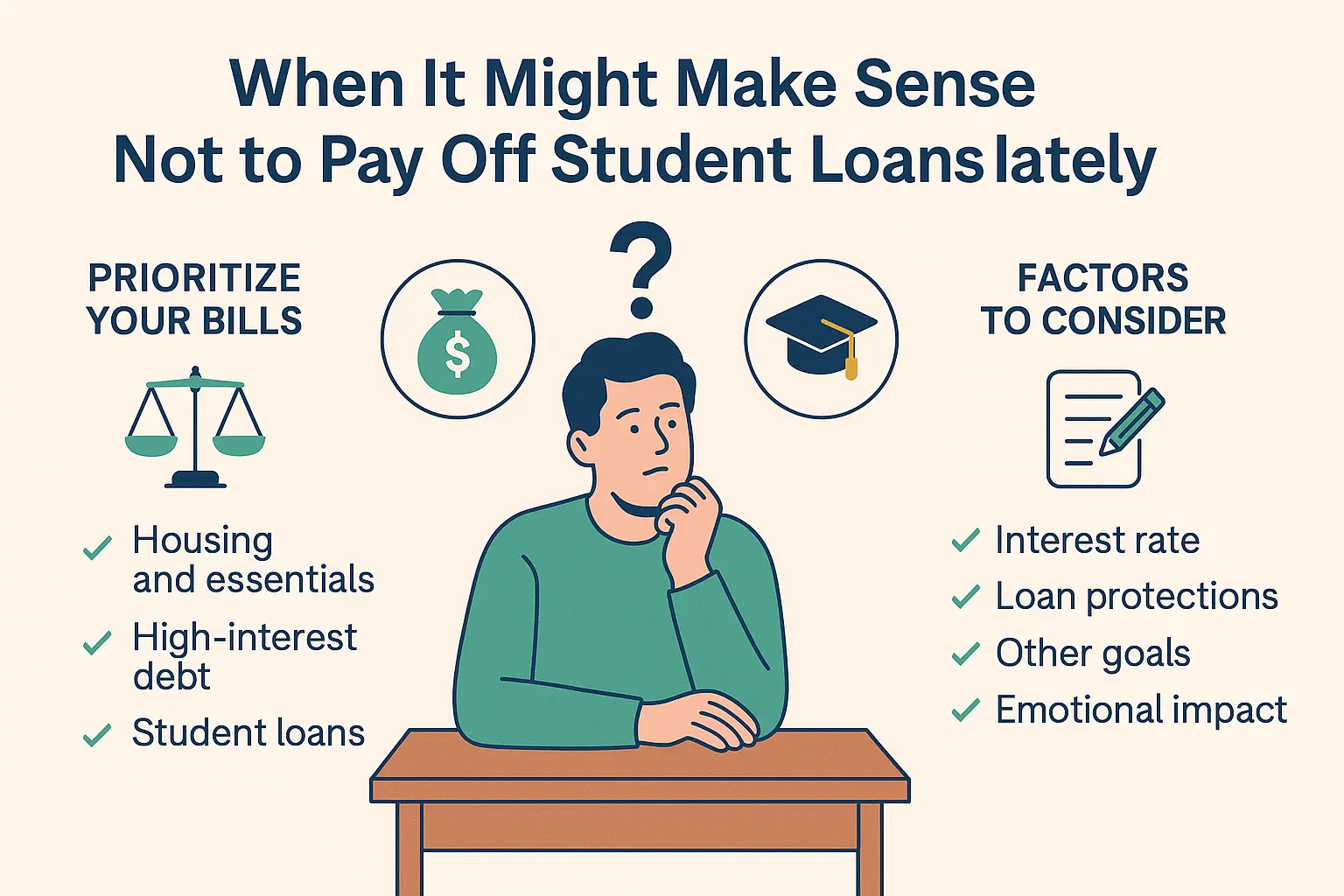

This post outlines how to prioritize your bills, when it may make sense not to pay student loans quickly, and what factors you should consider in building a thoughtful, long-term repayment strategy.

As a financial planner based in Santa Rosa, California, I’m familiar with the financial challenges many professionals, educators, and public service workers in the North Bay face including how to manage student loans while planning for home ownership and family goals.

Not All Debt Is Equal: Start With Strategic Prioritization

If you’re juggling multiple bills and limited resources, here’s one of the most important rules: not all debts carry the same consequences if unpaid.

Here’s a rough priority order based on consequences:

- Housing (mortgage or rent): Missing payments here could result in foreclosure or eviction.

- Auto loans: Missing payments can lead to repossession, affecting your ability to get to work.

- Essential utilities & insurance: Losing water, electricity, or medical coverage could cause real hardship.

- Secured debt (like home equity loans): These are tied to collateral.

- Unsecured consumer loans: These might go to collections, but generally don't threaten housing or transportation.

- Student loans: While important, they may offer repayment and relief options not available with other types of debt, particularly for federal loans.

This isn’t to suggest student loans don’t matter. But if paying them causes you to fall behind on housing, transportation, or critical needs, that’s a warning sign. Your debt plan needs to start with survival, then strategy.

When Paying Off Student Loans Slowly Can Be Smart

If your student loan interest rate is low, and you have alternative uses for the cash that are more productive, it may make sense to stretch out your repayment timeline.

Here’s an example:

Let’s say your federal student loan interest rate is 2.75% (rate for undergraduates in 2020–21, per educationdata.org). In Fall 2023, the 10-year U.S. Treasury yield was over 4.5% (according to the www.multpl.com).

Instead of paying off a 2.75% loan early, some borrowers may choose to invest in Treasuries or high-quality corporate bonds, which can yield 4–5% or more. These high-quality bond investments could outperform the cost of the loan.

In this context, carrying student debt while investing elsewhere may represent a rational financial arbitrage.

Of course, this assumes:

- You’re comfortable with investment risk

- You have stable income and liquidity

- You’re not emotionally burdened by the loan itself

Can You Pay Off a Student Loan Early Without Penalty?

For most borrowers, yes — federal and private lenders typically don’t charge fees for early payoff. However, paying early isn’t always the most strategic move if your interest rate is low or you’re eligible for forgiveness programs.

Risk Tolerance and Financial Personality Matter

This strategy doesn’t work for everyone.

Some people are psychologically debt-averse, and would rather pay off a loan with a 3% rate to feel better. Others are comfortable carrying debt and focused on maximizing long-term net worth.

Understanding your financial personality is key. If seeing a balance stresses you out or makes you lose sleep, the emotional ROI of becoming debt-free may outweigh the financial math.

Comparing Loan Types and Rates

To make an informed decision, you need to understand what your loans actually cost.

Here are some average interest rate ranges from the past decade as of Summer 2025:

| Loan Type | Average Interest Rate (Range) |

|---|---|

| Federal Student Loan | ~2.75% to 9.0% |

| Auto Loan (48-month) | ~4.0% to 8.5% |

| 30-Year Mortgage | ~2.65% to 7.75% |

Sources:

Infographic created using AI with support from OpenAI’s ChatGPT.

Depending on your specific loan rates, it might make more sense to prioritize mortgage or auto payments over student loans, especially if student loans are federally backed and have more flexible repayment terms.

Federal Loan Protections and Flexibility

Federal student loans come with built-in relief features designed to provide flexibility during times of financial strain or long-term planning:

- Income-Driven Repayment (IDR): Monthly payments are based on income and family size, helping keep payments manageable.

- Deferment and Forbearance: These allow you to temporarily postpone or reduce payments during periods of financial difficulty.

- Public Service Loan Forgiveness (PSLF): Forgives the remaining balance on Direct Loans after 120 qualifying monthly payments while working full-time for a qualifying government or nonprofit employer.

These features make it possible to pause or reduce student loan payments without immediately damaging your financial health, especially if you’re prioritizing housing, transportation, or emergency needs.

About Public Service Loan Forgiveness (PSLF)

If you’re employed by a U.S. federal, state, local, or tribal government or a qualified not-for-profit organization, you may qualify for PSLF. Here's how it works:

- You must make 120 qualifying monthly payments

- Payments must be made under an income-driven repayment plan or the 10-year Standard Plan

- You must be working full-time for a qualifying employer at the time of each payment and when applying for forgiveness

- Only Direct Loans are eligible; FFEL and Perkins loans must be consolidated into a Direct Consolidation Loan

- Payments do not need to be consecutive

Borrowers can use the PSLF Help Tool to determine employer eligibility, submit forms, and track qualifying payments.

In this scenario, choosing not to pay more than the minimum or not accelerating payoff isn’t procrastination. It’s a strategic decision aligned with a forgiveness plan.

Many borrowers ask, “Are there penalties for paying off student loans early?” For federal loans and most private loans, the answer is no—so paying extra can help reduce interest and shorten your repayment timeline.

For more details, visit the official source: studentaid.gov – Public Service Loan Forgiveness (PSLF)

Repayment Strategy Options

How should you prioritize which debts to pay?

Here are a few common approaches, and when they may make sense:

1. Highest-Interest First (Avalanche Method)

- Focuses on minimizing interest paid

- Best if you’re motivated by math and long-term savings

2. Smallest Balance First (Snowball Method)

- Focuses on behavioral wins and momentum

- Best if you need psychological motivation

3. Risk-Managed Strategy

- Prioritize essential secured debts (home, auto), then work down

- Best if your goal is financial security first, then growth

There’s no universal answer. A smart debt strategy combines numbers and emotions, tailoring repayment to your lifestyle, goals, and risk tolerance.

Should You Ever Stop Paying a Student Loan Altogether?

There are rare cases where people choose not to repay their student loans, not due to negligence, but as part of a larger strategy or life hardship. Here’s how to think about it:

- Deferment or forbearance can make sense in tough economic conditions, especially with federal loans

- Bankruptcy generally won’t eliminate student loans

- Deliberate default has major consequences: damaged credit, wage garnishment, and collection fees

If you're considering not paying a loan at all, seek financial counseling. There may be less damaging alternatives that preserve your financial stability.

If you're looking for a fee-only financial advisor in Santa Rosa, at Trusted Path Wealth Management, I work closely with clients to integrate debt management into broader financial planning strategies that align with their life goals.

Learn more about how I work with clients →

Final Thoughts

Student loans don’t always have to be the top priority, especially when their rates are low, and you have higher-impact uses for your money.

In some cases, choosing not to pay extra, or even temporarily pausing repayment, may be a reasonable strategy depending on your circumstances

But this decision should never be made in isolation. It should be part of a holistic financial plan that considers:

- Your full debt profile

- Your income stability and emergency reserves

- Your long-term goals (retirement, home purchase, giving, etc.)

- Your emotional relationship with debt

If you’re unsure about how to prioritize your debts or whether to accelerate your student loan payments, a conversation with a fee-only financial planner in Santa Rosa may help you sort through the options and design a strategy that reflects your life.