I am not going to tell you to invest all your money in Roth IRAs by paying taxes now so that you won’t pay any taxes on IRA income in retirement.

Instead, we will discuss a scenario where a couple has a mix of taxable accounts, Roth IRAs, Traditional IRAs, and Social Security benefits.

We’ll explore how it’s possible to generate $100,000 in retirement income without tapping into Roth IRA withdrawals; potentially resulting in $0 federal income tax.

This discussion will focus exclusively on federal income taxes. In California, dividends, IRA withdrawals, and capital gains are generally taxed as ordinary income, unlike federal treatment where some of these can qualify for 0% rates. This means John & Mary’s scenario could still trigger state taxes even if federal taxes are $0.

Let’s talk about a somewhat realistic scenario.

Meet John & Mary

- Age: 66

- Filing status: Married filing jointly

Baseline: If John & Mary Were Still Working

Let’s first look at the federal and FICA taxes they would owe if their entire $100,000 income came from W-2 wages.

Scenario: John & Mary still work, earning $100,000 W-2 wages in 2025.

2025 Standard Deductions for Age 65+ Married Filing Jointly

Base standard deduction: $31,500

(NerdWallet, Fidelity, Kiplinger)

New senior deduction (2025–2028): $12,000 total ($6,000 each spouse)

(IRS One Big Beautiful Bill)

Existing additional senior deduction: $3,200 (both spouses combined)

(2025 Form 1040-ES, IRS Form 1040-ES PDF)

Total standard deductions:

$31,500 + $12,000 + $3,200 = $46,700

Taxable income calculation

| Item | Amount | Notes |

|---|---|---|

| Gross W-2 Income | $100,000 | |

| Less: Standard Deductions | -$46,700 | Total of all deductions |

| Taxable Income | $53,300 |

2025 Federal Income Tax Brackets (Married Filing Jointly)

| Taxable Income Range | Tax Calculation | Tax Rate |

|---|---|---|

| $0 – $23,850 | 10% of taxable income | 10% |

| $23,851 – $96,950 | $2,385 + 12% of amount over $23,850 | 12% |

| $96,951 – $206,700 | $11,157 + 22% of amount over $96,950 | 22% |

| $206,701 – $394,600 | $35,302 + 24% of amount over $206,700 | 24% |

| $394,601 – $501,050 | $80,398 + 32% of amount over $394,600 | 32% |

| $501,051 – $751,600 | $114,462 + 35% of amount over $501,050 | 35% |

| Over $751,600 | $202,154.50 + 37% of amount over $751,600 | 37% |

Source: IRS Revenue Procedure 2024-40, Table 1 - Section 1(j)(2)(A)

Example: Calculating Federal Income Tax on $53,300 Taxable Income

First $23,850 taxed at 10%:

$23,850 × 10% = $2,385

Remaining amount:

$53,300 − $23,850 = $29,450 taxed at 12%:

$29,450 × 12% = $3,534

Total Federal Income Tax:

$2,385 + $3,534 = $5,919

Additional Payroll Taxes (FICA)

Social Security tax is 6.2% on wages up to the 2025 limit of $160,200

Calculation on $100,000 wages:

$100,000 × 6.2% = $6,200

Source: IRS Tax Topic 751 - Social Security and Medicare Withholding Rates

Total Taxes Paid (Federal Income + FICA)

| Tax Type | Amount |

|---|---|

| Federal Income Tax | $5,919 |

| FICA (Social Security) | $6,200 |

| Total Taxes | $12,119 |

Summary

John & Mary’s effective combined federal income and FICA tax on $100,000 wages in 2025 is approximately $12,119, after applying all standard and senior deductions.

Retirement: If John & Mary Were Retired - The $0 Tax Scenario

Step 1: Start with Social Security Income

Now let’s say the same couple is retired and wants to generate $100,000/year in retirement income. One of the advantages of planning is that you might have multiple options to generate this income while managing taxes effectively.

Let’s consider this couple’s situation:

Social Security income: $5,000/month, which totals $60,000/year

Total net worth of $2.8 million spread across:

$800,000 in a taxable stock portfolio (index fund ETF) with a 2% annual dividend yield

(all dividends are qualified dividends, no capital gains generated by the index fund ETF)

Cost basis of the taxable portfolio: approximately $400,000 (long-term basis assumed for this example)

$750,000 balance in John’s Traditional IRA

$750,000 balance in Mary’s Traditional IRA

$250,000 balance in John’s Roth IRA

$250,000 balance in Mary’s Roth IRA

- Goal: Generate $100,000/year in retirement income

Taxability of Social Security Benefits

Per IRS guidelines:

For married couples filing jointly, the provisional income is calculated as:

½ of combined Social Security benefits + all other combined income

If provisional income is:

Between $32,000 and $44,000, up to 50% of Social Security benefits may be taxable

Over $44,000, up to 85% of Social Security benefits may be taxable

Using the Social Security Benefits Worksheet (IRS Form 1040 Instructions), we calculate:

For educational purposes only; does not include state taxes.

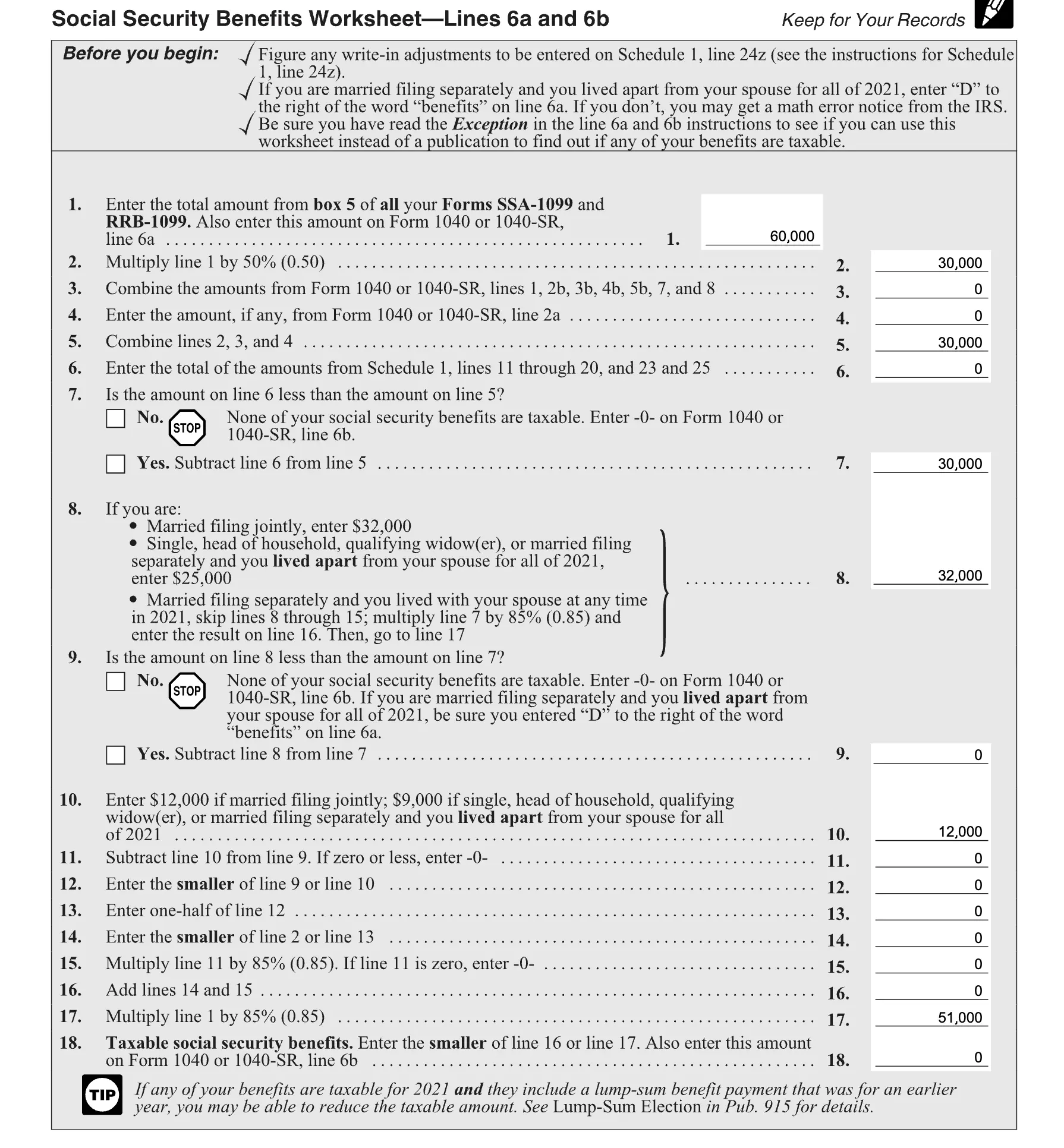

Since their provisional income is below $32,000 (because initially, Social Security is the only income), none of their Social Security benefits are taxable at this point.

Summary so far:

Income from Social Security: $60,000/year

No federal income tax on Social Security benefits at this stage

Step 2: Add Dividend Income

Now let's look into income and federal income tax from dividend income:

Couple has $800,000 stock portfolio invested in an index fund with an annual dividend yield of 2%.

2% of $800,000 generates $16,000 dividend income.

Now there are two income sources:

$60,000 from Social Security income

$16,000 from dividend income

Total income: $76,000

This increase is likely to make some of the Social Security income taxable. Let’s check:

For educational purposes only; does not include state taxes.

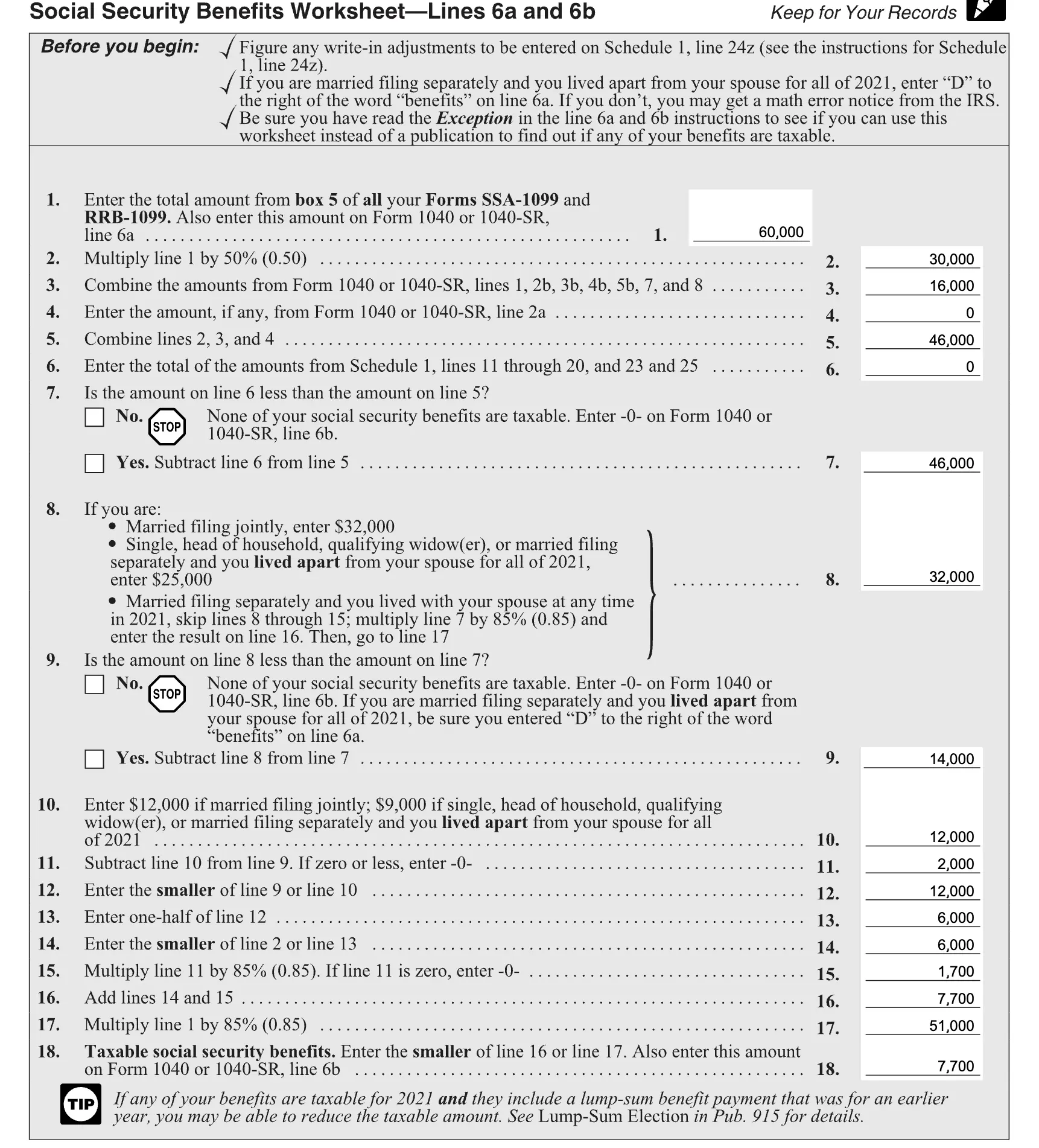

Using the Social Security Benefits Worksheet—Lines 5a and 5b after adding $16,000 dividend income,

$7,700 of Social Security benefits become taxable.

Adding $16,000 dividend income, the couple has a total taxable income of:

$7,700 (taxable Social Security) + $16,000 (dividends) = $23,700

This total income is still less than the standard deduction of $46,700, so the federal income tax remains:

$0 on $76,000 total income.

Step 3: Add IRA Withdrawals

We still need about $24,000 more income to reach the $100,000 retirement income goal.

We might choose to withdraw $15,000 from a Traditional IRA.

Now the couple has three income sources:

| Income Source | Amount |

|---|---|

| Social Security Income | $60,000 |

| Dividend Income | $16,000 |

| Traditional IRA Withdrawal | $15,000 |

This increases the taxable portion of Social Security benefits.

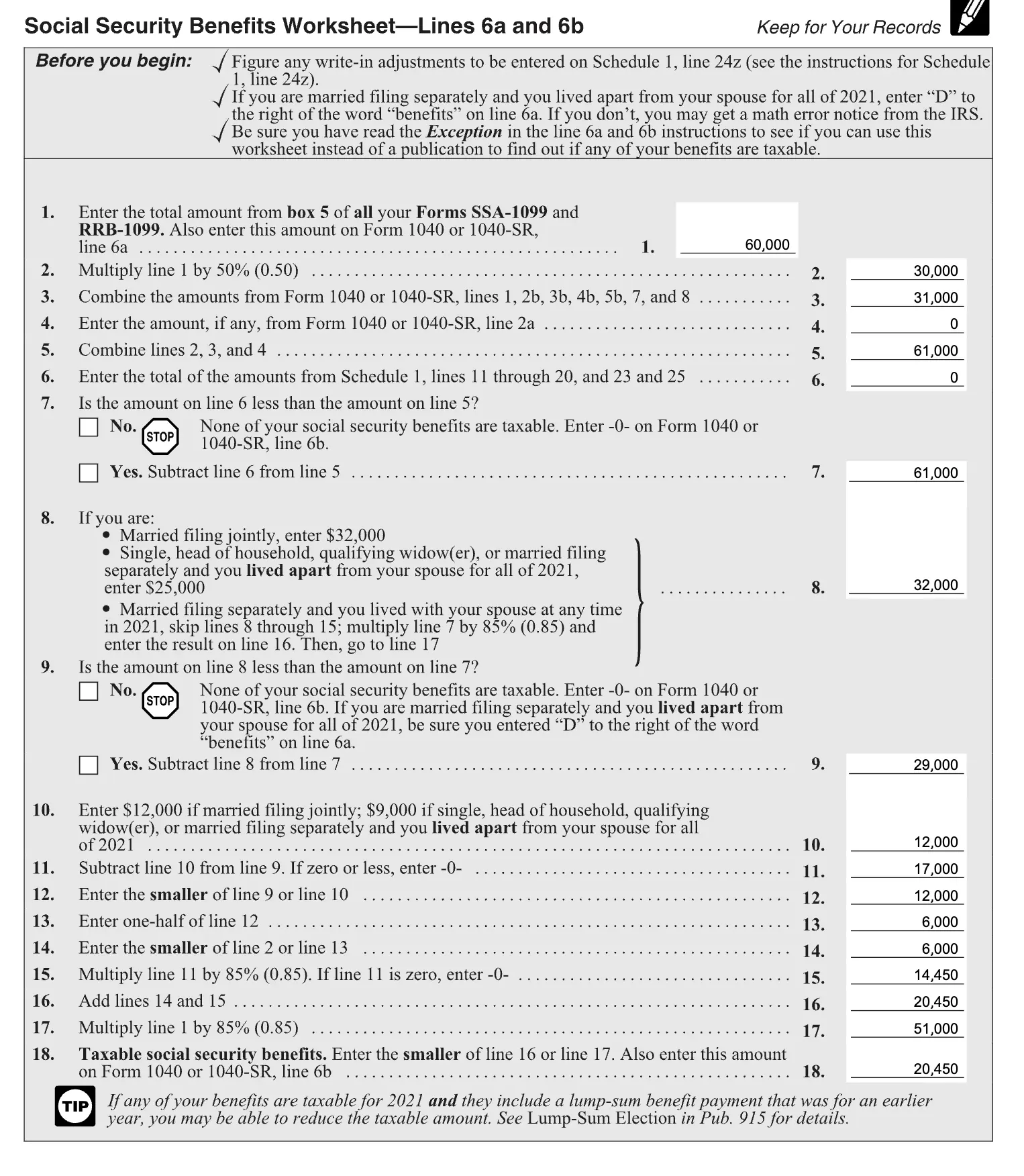

Using the Social Security Benefits Worksheet—Lines 5a and 5b

For educational purposes only; does not include state taxes.

| Description | Amount |

|---|---|

| Taxable Social Security Benefits | $20,450 |

| Total income for tax purposes | $51,450 |

| (Calculated as $16,000 dividend income + $15,000 IRA withdrawal + $20,450 taxable Social Security) |

Calculating taxable income:

| Calculation | Amount |

|---|---|

| Total income for tax purposes | $51,450 |

| Minus: Standard deduction (2025) | $46,700 |

| Taxable income | $4,750 |

Per IRS Publication 505 and IRS Revenue Procedure 2024-40:

For 2025, the maximum zero capital gains tax rate for Married Filing Jointly is up to $96,700 of taxable income.

Since qualified dividends and long-term capital gains are treated similarly for federal income tax purposes, and the taxable income is only $4,750,

All qualified dividends and long-term capital gains are taxed at 0%, resulting in $0 federal income tax on this income.

Step 4: Add Income from Selling Some Taxable Assets

To fully reach their $100,000 retirement income goal, the couple sells some taxable assets for $9,000 proceeds.

Now the income sources are:

| Income Source | Amount |

|---|---|

| Social Security Income | $60,000 |

| Dividend Income | $16,000 |

| Traditional IRA Withdrawal | $15,000 |

| Income from selling some taxable assets | $9,000 |

Assuming a 50% cost basis, this results in $4,500 of long-term capital gains (LTCG, profits from selling investments you’ve held more than a year).

This affects the taxable portion of Social Security benefits.

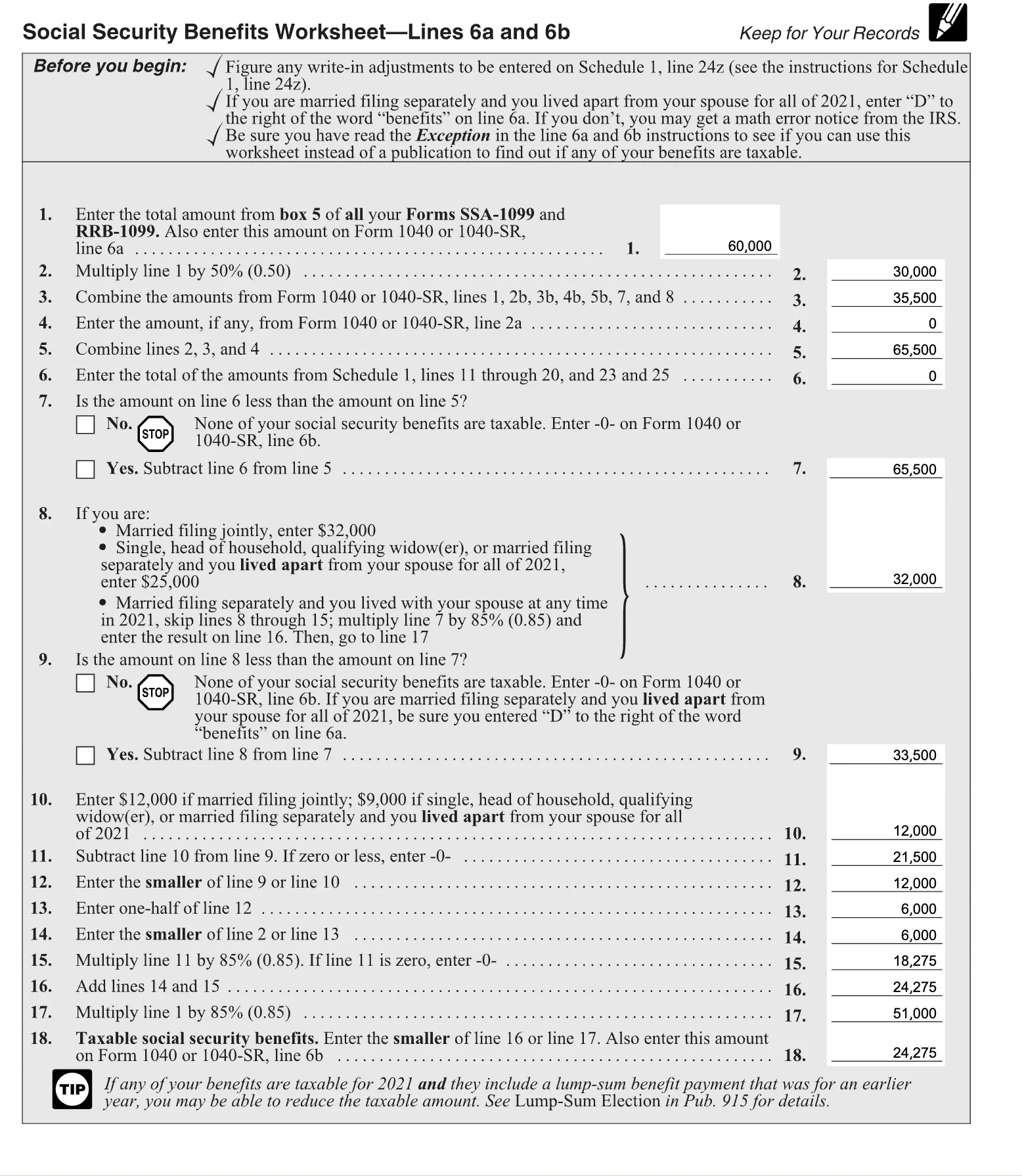

Using the Social Security Benefits Worksheet

For educational purposes only; does not include state taxes.

| Description | Amount |

|---|---|

| Taxable Social Security Benefits | $24,275 |

| Total income for tax purposes | $59,775 |

| (Calculated as $16,000 dividend + $15,000 IRA + $24,275 taxable Social Security + $4,500 LTCG) |

Calculating taxable income:

| Calculation | Amount |

|---|---|

| Adjusted Gross Income (AGI) | $59,775 |

| Minus: Standard deduction (2025) | $46,700 |

| Taxable income | $13,075 |

Per IRS Revenue Procedure 2024-40, for Married Filing Jointly in 2025:

The maximum zero capital gains tax threshold is $96,700 of taxable income.

Since their taxable income $13,075 is well below the $96,700 threshold,

The long-term capital gains and qualified dividends remain taxed at 0%, resulting in $0 federal income tax on this income.

For educational purposes only; does not include state taxes.

Is $0 Federal Tax Always the Goal?

Even though John and Mary could pay $0 federal tax in this scenario, is that always the best strategy? The answer isn’t black and white.

Tax efficiency over a lifetime often means planning beyond just minimizing tax this year. Sometimes paying some tax now may save more tax later.

For example, taking larger IRA distributions during low-tax years may reduce the size of Required Minimum Distributions (RMDs) in future, potentially lowering future tax bills.

Tax gain harvesting: selling investments to realize gains during low tax years, may reset the cost basis and reduce capital gains taxes later.

IRMAA (Income-Related Monthly Adjustment Amount) affects Medicare premiums based on income, so managing taxable income may help avoid higher Medicare surcharges.

Roth conversions during low-income years might let you pay tax now at a lower rate, resulting in tax efficiency and less RMD pressure in retirement.

In short, a balanced tax strategy looks at current and future tax impacts, not just minimizing tax today.

The Bottom Line

By carefully blending Social Security, qualified dividends, modest IRA withdrawals, and long-term capital gains, it’s possible to meet a $100,000 retirement income target with zero federal income tax.

But optimizing tax efficiency over your entire lifetime, not just in a single year, may lead to better long-term outcomes.

Key Takeaways

- Structuring income sources may minimize or even eliminate federal income taxes in retirement.

- Social Security, qualified dividends, and long-term capital gains may be taxed at 0% within certain limits.

- Completely avoiding tax in low-income years might not be optimal. Some tax now may mean less tax later.

- Watch for IRMAA (Medicare premium surcharges) when planning withdrawals.

Further Reading

- IRS – Social Security Benefits May Be TaxableRead article →

- IRS 2025 Tax Brackets – Rev. Proc. 2024-40Read article →

- Tax-Efficient Withdrawal Strategies in RetirementReduce lifetime taxes and extend your portfolio. Learn the optimal withdrawal order for taxable, tax-deferred, and Roth accounts, plus Roth conversion timing and Medicare IRMAA planning.Read article →