What California Retirees and Federal Policy Watchers Should Know

In California, Social Security benefits are not taxed. But at the federal level, and depending on your income, they might be. With the newly enacted "One Big Beautiful Bill" now in effect, understanding how your Social Security could be taxed (or not) could be especially helpful right now.

A Brief History of Social Security

Social Security has become one of the most essential pillars of retirement planning in the U.S. Here’s a quick overview of how it came to be:

1935: The Social Security Act was signed into law by President Franklin D. Roosevelt, originally offering retirement benefits to a limited number of workers.

1940: First regular monthly benefit check issued to Ida May Fuller: $22.54.

1950s to 1970s: Major expansions, including survivor benefits, disability insurance, and Medicare integration.

1983: Social Security began to be partially taxed under President Reagan’s reforms. Benefits became taxable based on income.

1993: Under President Clinton, the taxable portion of benefits increased, affecting more middle-income retirees.

Today: Social Security is funded through payroll taxes (6.2% each from employer and employee). Depending on income, up to 85% of Social Security benefits may be taxed federally.

Source: Social Security History

When Did Social Security Start Getting Taxed?

Although Social Security benefits were originally tax-free, that changed with the Social Security Amendments of 1983.

Since then, if your income exceeds certain thresholds, up to 50% or even 85% of your Social Security benefits may be subject to federal income tax.

How It Works Today

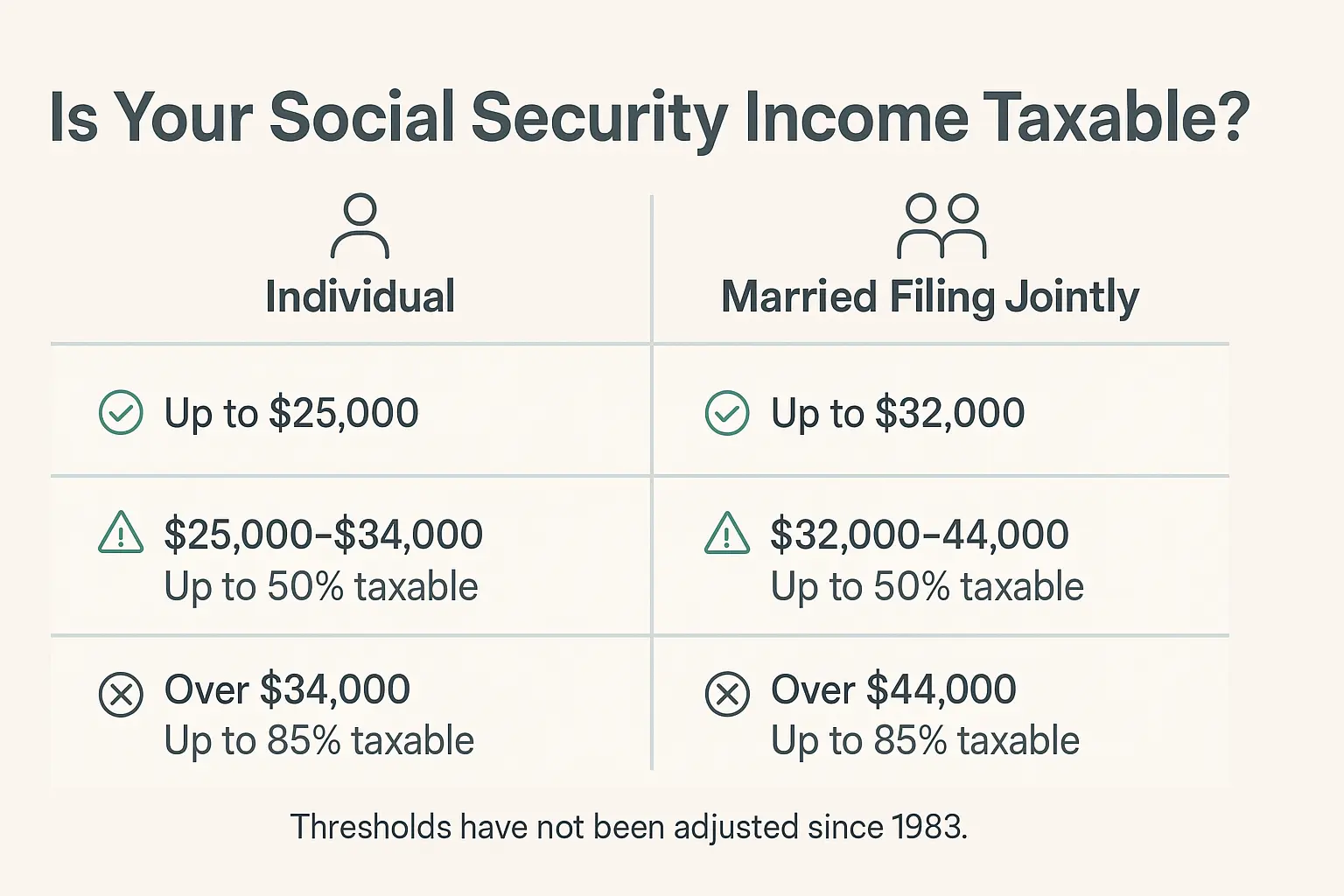

Here’s how much of your Social Security may be taxed, based on your filing status:

Image generated with AI assistance from Copilot, and is for educational purposes only. It does not reflect official IRS content.

Combined income = Adjusted Gross Income (AGI) + nontaxable interest + 50% of your Social Security benefits

Here’s how much of your Social Security may be taxed, based on your filing status:

If you file as an individual:

- Up to $25,000: No tax

- $25,000 to $34,000: Up to 50% of benefits may be taxable

- More than $34,000: Up to 85% may be taxable

If you file a joint return:

- Up to $32,000: No tax

- $32,000 to $44,000: Up to 50% of benefits may be taxable

- More than $44,000: Up to 85% may be taxable

These rules apply to retirement, survivor, and disability benefits, but not to Supplemental Security Income (SSI), which remains non-taxable.

A Key Detail Many Miss

The income thresholds of $25,000 (individual) and $32,000 (joint filers) have never been adjusted for inflation since they were first introduced in 1983.

As a result:

- In 1983, only about 10% of Social Security recipients paid federal taxes on their benefits.

- Today, that number is closer to 56% (source: SSA.gov).

As a result, even retirees with moderate income may find that a portion of their Social Security benefits is included in their federal taxable income.

It’s a common surprise. Some people might assume that their Social Security benefits won’t be taxed at all, but under current rules, some of those benefits may be partially taxable in retirement.

Avoid these common missteps that may trip up many retirees:

Common Retirement Mistakes, and Strategies That May Help You Prepare

New Deduction for Seniors (2025 to 2028)

The One Big Beautiful Bill Act, enacted in 2025, introduced a new tax deduction aimed at providing relief for older Americans.

An additional $6,000 deduction is available for taxpayers age 65 or older

Married couples filing jointly may claim up to $12,000 if both spouses qualify

This deduction is in addition to the existing standard deduction for seniors

Phase-out begins at:

$75,000 modified adjusted gross income (MAGI) for individuals

$150,000 MAGI for joint filers

The deduction applies whether you itemize or take the standard deduction

To qualify:

Must be 65 or older by the end of the tax year

Social Security Numbers of eligible individuals must be included

Married couples must file jointly to claim the full deduction

IRS – One Big Beautiful Bill Act Tax Deductions for Working Americans and Seniors

This new deduction could reduce retiree's overall taxable income, which may help lower the portion of Social Security benefits included in retiree's federal taxable income.

Want more details on how this new legislation could affect retiree's retirement taxes?

2025 Tax Changes: What the One Big Beautiful Bill Means for You

How Much Could This Deduction Actually Save You?

The value of the $6,000 (or $12,000 for couples) senior deduction depends on retiree's tax bracket. Here's a breakdown of potential tax savings based on 2025 federal tax rates:

Single Filers (Age 65+)

| Tax Bracket | $6,000 Deduction Saves You |

|---|---|

| 10% | $600 |

| 12% | $720 |

| 22% | $1,320 |

| 24% | $1,440 |

Married Filing Jointly (Both 65+)

| Tax Bracket | $12,000 Deduction Saves You |

|---|---|

| 10% | $1,200 |

| 12% | $1,440 |

| 22% | $2,640 |

| 24% | $2,880 |

What this means:

The higher retiree's marginal tax rate, the more valuable the deduction becomes. Even for lower-income seniors, this deduction provides meaningful savings, especially when combined with the existing standard deduction.

Keep in mind: The deduction phases out starting at $75,000 (single) or $150,000 (joint), so high-income seniors may receive only a partial benefit or none at all.

How and when you withdraw money in retirement can significantly impact retiree's taxes:

Tax-Efficient Withdrawals: How You Take Money in Retirement Matters More Than You Think

Let’s Look at a Hypothetical Example

Married Couple, Both 67 Years Old

- Social Security Income: $36,000/year

- IRA Withdrawals (Taxable): $20,000/year

- Filing Status: Married Filing Jointly

Step 1 – Combined Income Calculation

To determine if Social Security benefits are taxable, calculate combined income:

Combined Income = IRA ($20,000) + 50% of Social Security ($18,000)

= $38,000 combined income

This puts the couple in the $32,000 to $44,000 range, meaning up to 50% of their Social Security may be subject to federal income tax.

Step 2 – Estimate Taxable Social Security

- Up to 50% of $36,000 = $18,000 potentially taxable

- Add $20,000 from IRA withdrawals

= $38,000 total taxable income before deductions

Step 3 – Apply Federal Deductions

- $32,300 – Standard deduction for married filing jointly, 65 or older (both spouses) – this is for year 2024. Check current info per Publication 501

- $12,000 – New senior deduction introduced in One Big Beautiful Bill in 2025 ($6,000 × 2)

Add those two to get the total.

Step 4 – Final Taxable Income

Since their taxable income is lower than their deductions,

could potentially have no federal income tax liability.

Based on this hypothetical example, the couple’s deductions exceed their income subject to federal taxation. This could result in zero federal tax liability.

This is a simplified estimate. Final tax owed can vary based on the exact taxable portion of Social Security, credits, and other deductions.

This example shows how the new senior deduction helps many retirees avoid federal tax, especially in California, where Social Security is not taxed at all.

California’s Tax Treatment of Social Security

Good news for California retirees:

California does not impose state income tax on Social Security benefits.

Unlike many other states, per California Tax Service Center, California fully exempts Social Security income from state income taxes, regardless of how much you receive.

What’s Exempt?

- Retirement benefits

- Spousal benefits

- Survivor benefits

- Disability benefits (SSDI)

Note: Supplemental Security Income (SSI) is not taxed federally or by California. It also does not count toward combined income for federal tax purposes.

For Californians, this means only federal taxes apply to retiree's Social Security.

Understanding federal rules and available deductions, like the new senior deduction may help retirees make informed tax decisions.

Looking for guidance from a local fiduciary advisor in Santa Rosa?

How a Solo Financial Advisor in Santa Rosa Builds Your Portfolio

This blog is for general educational purposes only and does not constitute legal or tax advice. Tax situations vary; please consult a qualified tax professional before making decisions.