At Trusted Path Wealth Management in Santa Rosa, California, we help navigate retirement transitions with personalized strategies. Whether you’re a few years away from retirement or already retired, knowing what not to do is just as important as knowing what to do.

In this post, we’ll cover some of the most common and costly mistakes you may make in retirement: many of which seem harmless in the early years, but may cause problems later. With professional guidance and careful planning, many of these issues can be addressed.

Let’s break them down, and more importantly, learn how to avoid them.

Should I Retire Without a Written Plan? No—Here’s Why

If you approach retirement with just a general sense of readiness but no clear, documented strategy, retirement may become a series of ad-hoc decisions. Without a plan for how to draw income, manage taxes, and adjust for longevity, you may face emotional spending or unnecessary frugality, miss tax-efficient opportunities, and overlook gaps in healthcare or estate planning.

A thoughtful retirement plan doesn’t need to be hundreds of pages, but it should coordinate your income sources, withdrawal order, investment risk, tax strategy, and legacy goals.

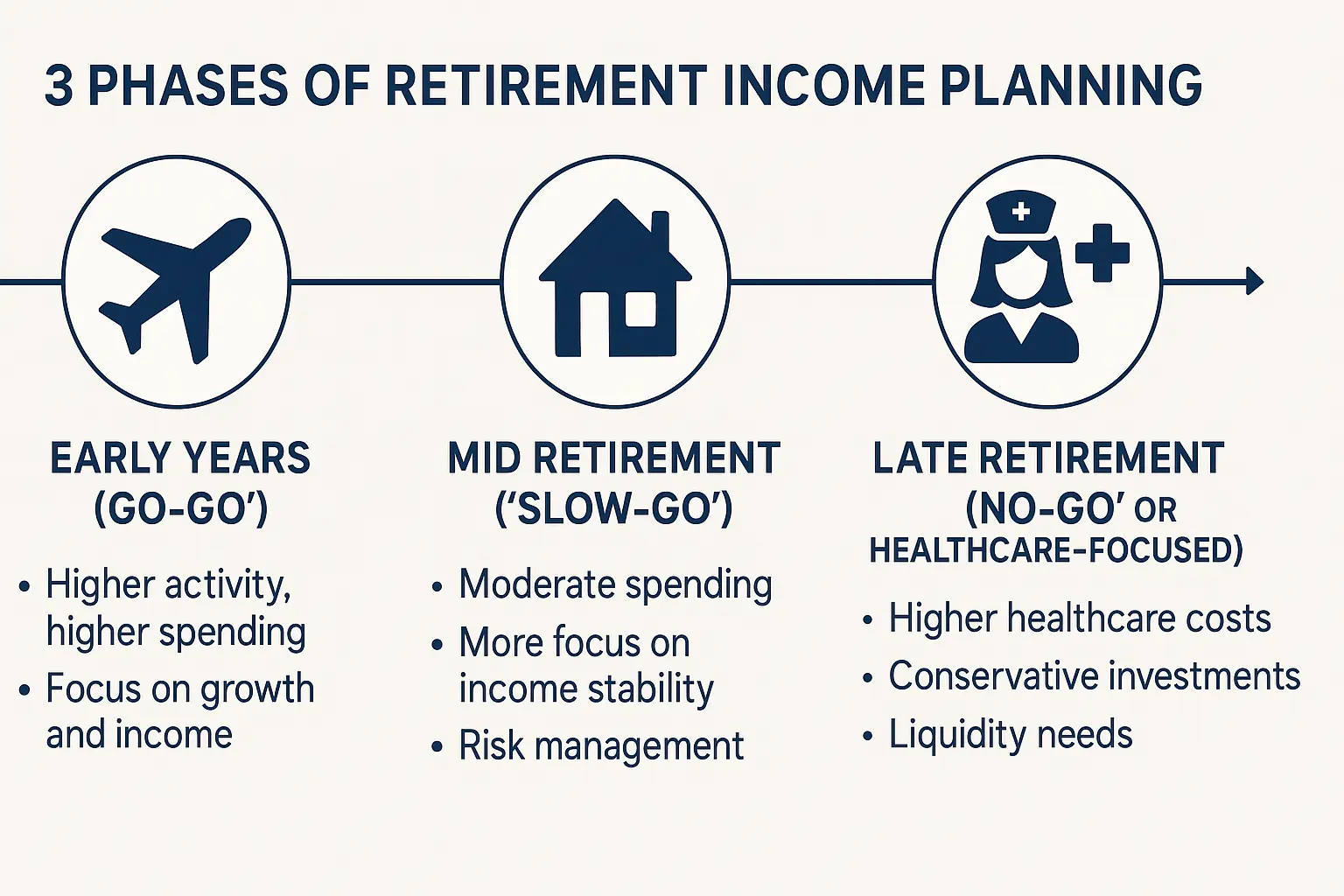

Tip: You may want to start with a written retirement income/withdrawal plan that maps out the stages of retirement: early "go-go" years, mid-retirement stability, and later healthcare-focused years. Plan to revisit it annually.

Image generated with AI assistance from Copilot. This image is for illustrative purposes only and does not reflect actual performance or specific financial outcomes

Should I Have a Withdrawal Strategy? Yes—It’s Often Your Biggest Opportunity

This is often the most impactful decision you make in retirement. Without a coordinated plan for which accounts to draw from, and when, you may not optimize tax-efficiency, trigger unintended Medicare IRMAA surcharges, or run out of money sooner than expected. The order and timing of your withdrawals can easily mean the difference between a sustainable 30-year retirement and one that falters in later years.

You may overlook the benefits of proactive planning around Required Minimum Distributions (RMDs). While RMDs are mandatory starting at age 73, it may be wise to withdraw more earlier, especially in low or no-tax years, such as the early retirement window before your Social Security or pension income begins. This may reduce your future RMDs and potentially keep you in a lower tax bracket longer.

You might also consider Roth conversions during these low-income years to build future tax-free income.

Another common oversight: donating to charity from a taxable account when you’re eligible for a Qualified Charitable Distribution (QCD) from an IRA. QCDs may satisfy your RMD and may reduce your taxable income while maximizing your charitable impact.

Tip: You may want to design a flexible, tax-efficient withdrawal plan early, and revisit it regularly. Consider Roth conversions and QCDs to optimize both your taxes and charitable giving.

More on this topic: Tax-Efficient Withdrawals: How You Take Money in Retirement Matters More Than You Think

Should I Claim Social Security at 62? Consider the Long-Term Impact

Many people claim Social Security at 62 simply because they can. But claiming early comes with a permanent reduction in your benefits: about 30% lower than if you wait until your Full Retirement Age (FRA) of 67 (for those turning 62 in 2025). While early claiming may be the right choice in some cases, it often locks in reduced lifetime income and limits your future flexibility.

Your benefit will increase if you delay claiming past your full retirement age: by about 8% for each full year, up to age 70. These are called delayed retirement credits and may substantially increase your benefit over time.

Source: Social Security Administration – When to Start Receiving Retirement Benefits (SSA.gov)

Tip: If you have good health and savings, you may want to consider delaying your Social Security to increase your lifetime benefits, but it's important to evaluate this within your full financial plan

More on this topic: A Few Reasons to Take Social Security Early at Age 62

Should I Ignore Inflation in Retirement? No—It Quietly Erodes Your Purchasing Power

Inflation quietly erodes your purchasing power. Over a 25 to 30 year retirement, a fixed income may not keep up, especially with rising healthcare, housing, and everyday expenses.

You may have heard a lot about investing in retirement to generate income, but chasing returns can lead to taking on unnecessary risk. Instead of focusing solely on income or growth, focus on your cash flow needs. There are two ways to generate gains: price appreciation and interest/dividends. A sustainable retirement strategy often blends both, but should always be rooted in your personal goals, risk tolerance, and timeline.

Do not underestimate TIPS (Treasury Inflation-Protected Securities). Though not as popular as other investments, TIPS are specifically designed to protect your investment from inflation, making them a vital tool in combating rising costs over time.

Equity may also be helpful in combating inflation over the long run, as businesses often pass increased costs onto consumers, which may be reflected in price appreciation.

Tip: Build in flexibility and inflation protection, but don’t take on risk you don’t need. Focus on your total income picture, not just one source of return.

More on this topic: Smart Tax Strategies for Retirement: A Guide to Tax-Efficient Planning

Should I Hold Too Much in Cash? Or Stay Too Aggressive? Finding Your Balance

After decades of saving, you may become overly cautious, keeping too much in cash or low-yield accounts. The problem? Cash loses value over time due to inflation, and may not generate enough income to support a 20–30 year retirement.

On the flip side, you may stay overly aggressive, leaving too much exposed to market volatility. A sharp downturn early in retirement, known as sequence of returns risk can potentially undermine your long-term strategy if you're drawing from investments during a market dip.

The key is finding the right balance for you. Your retirement portfolio should be designed to generate stable income, preserve your capital, and grow moderately to keep pace with inflation.

Tip: You may want to align your portfolio with your time horizon, income needs, and risk tolerance. A mix of cash, bonds, and equities; thoughtfully allocated can help support a more stable retirement.

- How a Solo Financial Advisor Builds Your Portfolio

- Tax-Efficient Asset Location: One Change, $2.1 Million More

Should I Overlook Tax Planning in Retirement? No—It Directly Affects Your Lifetime Wealth

Taxes do not stop in retirement and without careful planning, they can take a bigger bite out of your income than expected. Your withdrawals from traditional IRAs and 401(k)s are taxed as ordinary income, and large distributions can push you into higher tax brackets or trigger Medicare premium surcharges (IRMAA). You may also miss opportunities in low-income years, like the early years of retirement before RMDs begin.

Strategic tax planning in retirement may add efficiency to your lifetime tax bill and help you preserve more of your wealth. This includes not just tax efficiency in income taxes, but also managing your capital gains, optimizing your account withdrawals, and taking advantage of tax-smart giving.

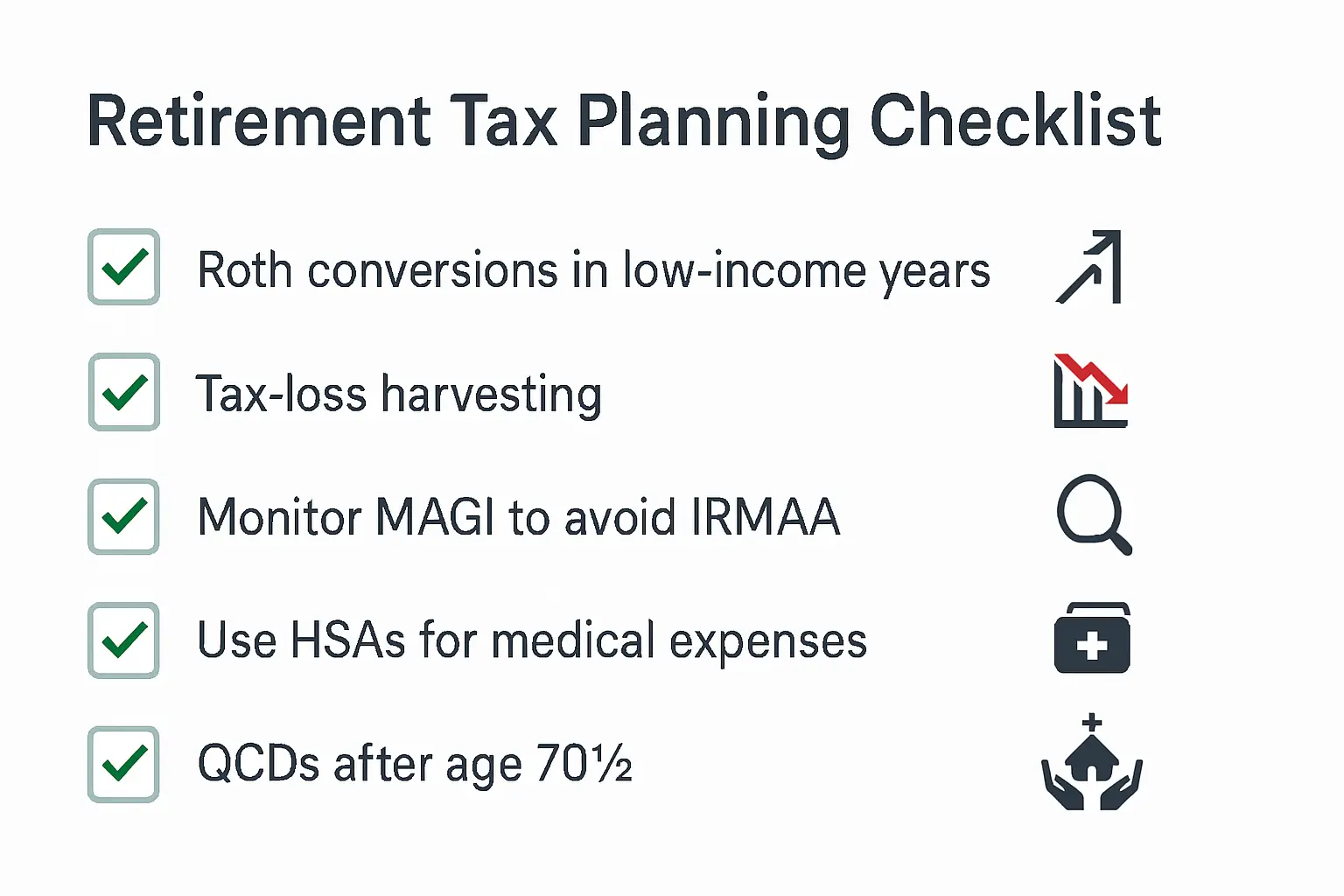

Tip: Depending on your tax situation, strategies like Roth conversions, tax-loss harvesting, or QCDs may offer advantages. Consult a tax advisor or financial planner to assess suitability.

Image generated with AI assistance from Copilot. This image is for illustrative purposes only and does not reflect actual performance or specific financial outcomes

More on this topic: Tax-Efficient Withdrawals: How You Take Money in Retirement Matters More Than You Think

Should I Plan for Average Life Expectancy? Or Plan Longer?

If you plan based only on average life expectancy, you may be underestimating your retirement timeline. About half of people might live longer than average. With improved healthcare and lifestyle habits, it’s not uncommon to live well into your 90s. Planning for only 20 years of retirement income may leave you short if your retirement lasts 30 years or more.

Longevity risk, the chance of outliving your money, is one of the most significant yet overlooked threats to your retirement security. It’s especially problematic if your spending is too high early on, your investment returns are lower than expected, or your healthcare costs rise significantly later in life.

Tip: It may be prudent to account for the possibility of living into your 90s or beyond. Your retirement strategy should support 30+ years of income, account for inflation and healthcare costs, and adapt as your needs evolve.

More on this topic: A Step-by-Step Guide to Retirement Planning

Should I Work With a Fiduciary Advisor? Consider It for Complex Decisions

Retirement decisions are complex, and working with a professional may provide you with perspective and support. Fiduciary advisors are legally obligated to act in your best interest under the Investment Advisers Act of 1940.

Rather than focusing on products or transactions, a fiduciary takes a holistic view of your financial life: covering your retirement income, tax strategy, healthcare planning, and estate considerations.

Tip: Look for an fiduciary, fee-only advisor who can serve as a long-term planning partner and may provide structured guidance and help you make informed decisions.

- What Is a Fee-Only Fiduciary Financial Advisor? Independent & Client-First Approach

- What Should I Look For in a Financial Advisor?

Wrapping Up: Avoidable Doesn’t Mean Obvious

Retirement is more than ending your career. It’s about navigating a complex web of financial decisions that affect your income, your taxes, and your peace of mind. While some mistakes are hard to see coming, most are avoidable with the right guidance and a forward-looking plan.

If you’re approaching or navigating retirement and want a second set of eyes on your plan, I’d be glad to discuss it with you.

Based in Santa Rosa, CA, I work with clients both locally and virtually. Start your path here:

Investment and tax strategies discussed are for informational purposes only and may not be suitable for all individuals. Consider consulting with a tax advisor or financial professional before acting on any strategy.

Updated December 14, 2025