When planning for retirement, one of the most important choices you may face is: “When should I start collecting Social Security?”

This decision may impacts your lifetime income, tax strategy, and even your spouse’s benefits. Whether you're weighing social security at 62 vs 70, wondering should i take social security at 67 or 70, or comparing social security at 66 vs 70, let's break down the key considerations and the pros and cons of starting at 62, 67, or 70.

Social Security Basics

Before diving into the pros and cons, it’s important to understand the basics of how Social Security works, since this foundation might help you make sense of the advantages and drawbacks of each claiming age.

How Benefits Are Calculated

Social Security calculates your primary insurance amount (PIA) based on your 35 highest-earning years, adjusted for inflation.

Think of your PIA as the baseline monthly Social Security benefit you would receive if you start collecting at your full retirement age.

For more ways to increase your Social Security benefits, consider strategies that complement your retirement portfolio.

Full Retirement Age (FRA)

Your full retirement age is typically 66–67, depending on your birth year. This is the age at which you receive 100% of your PIA.

Full retirement age has shifted over time as Social Security rules and life expectancy have changed.

Early or Delayed Benefits

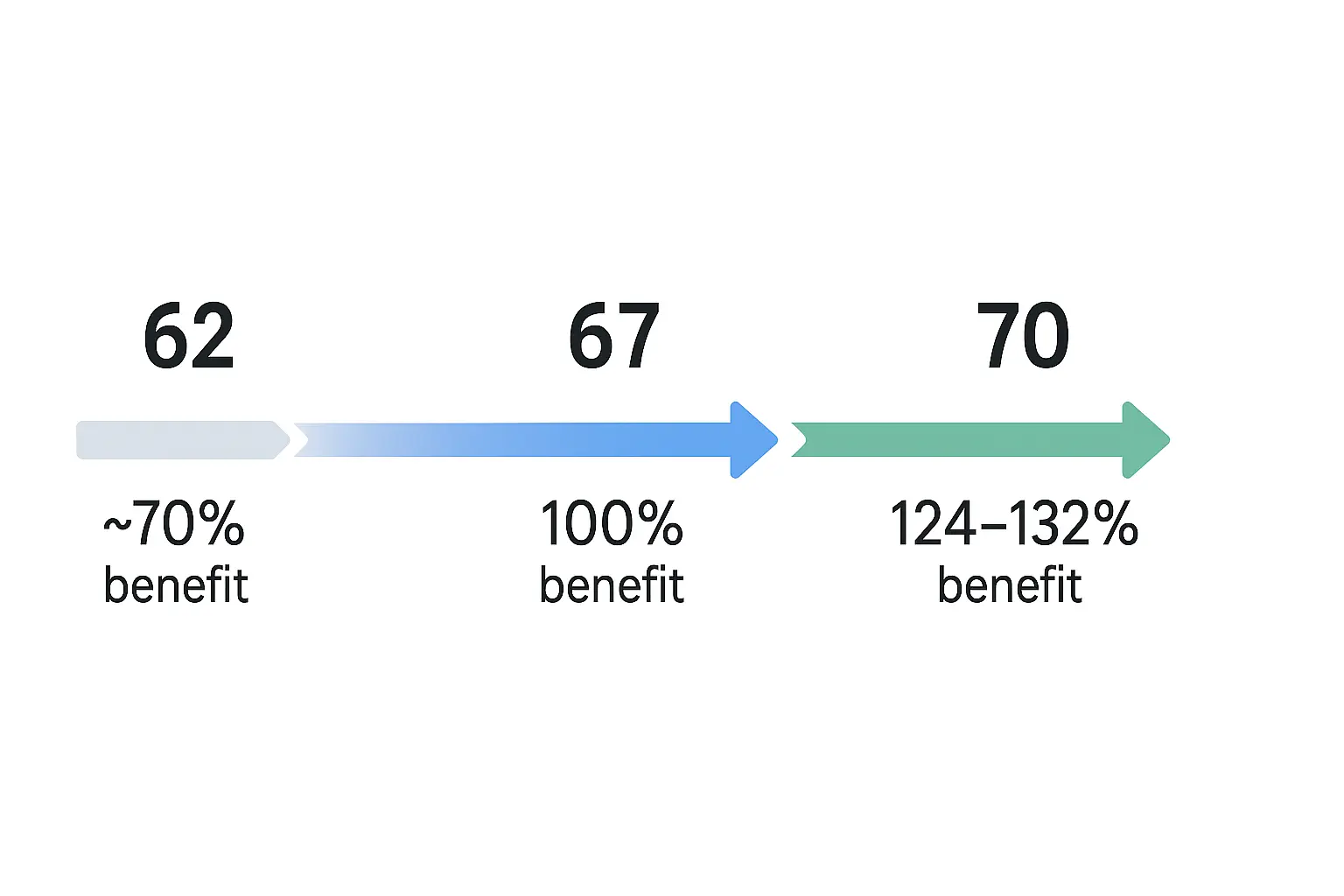

You can start collecting Social Security as early as age 62, but the trade-off is that your monthly check may be smaller. On average, starting at 62 means you’ll only get about 70% of your full benefit for the rest of your life.

Waiting until your full retirement age (66–67 depending on birth year) gives you 100% of your benefit.

If you wait even longer, your monthly check gets a boost. For every year you delay past full retirement age, you earn “delayed retirement credits.” For most people born after 1943, this means about an 8% increase per year, up until age 70. After 70, there’s no extra benefit to waiting.

For details and exact numbers by birth year, check the SSA reduction chart and the SSA delay calculator.

Image generated with AI assistance from OpenAI for educational purposes only.

Pros & Cons of Collecting at 62

Downsides

- Lower monthly benefits: Collecting early may lock in a permanent reduction. For example, starting at 62 may reduce your benefit to about 70% of your PIA.

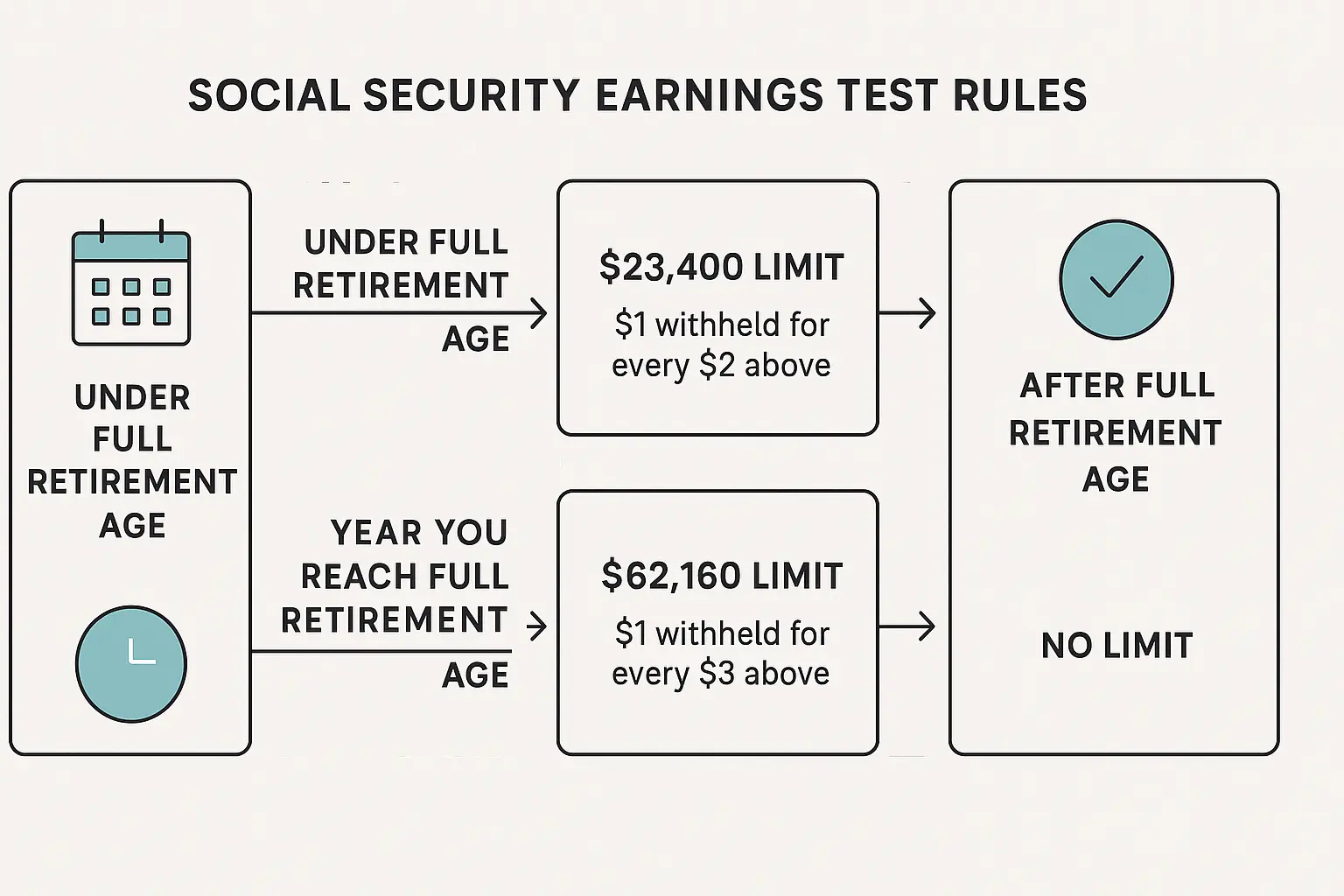

- Working while collecting early: If you start Social Security before FRA and keep working, some benefits may be temporarily withheld if your income is above certain limits.

- Under full retirement age for the year: In 2025, you can earn up to $23,400 without reductions. Above that, Social Security withholds $1 for every $2 you earn over the limit.

- Year you reach full retirement age: Only earnings before your birthday month are counted. In 2025, the limit is $62,160. Benefits are withheld $1 for every $3 above this limit.

- After reaching full retirement age: No limits. Earnings do not affect your full benefits.

Image generated with AI assistance from OpenAI for educational purposes only.

It’s also important to understand how Social Security is taxed in California and federally to make the most of your benefits.

According to the Social Security Administration, withheld benefits are credited back when you reach FRA, so you don’t permanently lose them.

- Impact on survivor benefits: Early collection may reduce the income available to a surviving spouse.

Benefits

- Immediate cash flow: May provide income right away if needed.

- Portfolio flexibility: Drawing Social Security earlier may reduce the need to withdraw from investments.

Coordinating your Social Security with other assets is easier with guidance from a Santa Rosa financial advisor who can build your retirement portfolio.

For more details, see the Social Security Administration guide on early retirement reductions.

Pros & Cons of Collecting at 70

Benefits

- Maximized Social Security: Monthly benefits may increase up to 24% higher than full retirement age.

- Higher income floor: Provides a stable income in later years, reducing longevity risk.

- Supports tax strategies: Deferring Social Security allows for more effective Roth conversions and lower taxable income in early retirement.

- Protection for spouse: If married, the surviving spouse may benefit from the higher income floor.

Working with an independent, fiduciary, fee-only financial advisor may ensure your Social Security strategy aligns with your long-term retirement plan.

Downsides

- Delayed gratification: Must wait longer to access benefits, which may require drawing from other sources.

- Uncertainty of lifespan: If you pass away before collecting, you forfeit the deferred benefits.

- Opportunity cost: Delaying may require using investment portfolio assets sooner, reducing compounding potential.

The Bottom Line

There is no one-size-fits-all answer.

Age 62 is best for immediate cash flow or short life expectancy.

Age 67 provides a balanced approach with full benefits at a moderate deferral.

Age 70 maximizes monthly benefits and longevity protection but requires delayed gratification.

The right choice depends on your health, life expectancy, spouse considerations, cash flow needs, and overall retirement plan. Consider consulting a financial advisor to coordinate Social Security with investments, taxes, and retirement income planning.

Image generated with AI assistance from OpenAI for educational purposes only.

Key Takeaways

Social Security can be collected at 62, 67, or 70.

Early collection reduces monthly benefits; delaying increases them through delayed retirement credits.

Delayed benefits may improve portfolio flexibility and support tax-efficient strategies.

Consider the impact on spousal and survivor benefits.

Health, life expectancy, and cash flow needs are central to timing your decision.

Avoid common pitfalls by reviewing frequent retirement mistakes related to claiming Social Security and withdrawals.

Coordinate your Social Security with your investment accounts for tax-efficient withdrawals in retirement.

If you’re looking for guidance, learn how to start working with a trusted financial advisor to make confident decisions.

Explore the services we offer for a comprehensive approach to retirement planning.

Learn more about what to look for in a financial advisor when planning Social Security and retirement strategy.

Updated December 18, 2025